EN EN

EUROPEAN

COMMISSION

Brussels, 14.10.2020

COM(2020) 953 final

REPORT FROM THE COMMISSION TO THE EUROPEAN PARLIAMENT AND

THE COUNCIL

on progress of clean energy competitiveness

{SWD(2020) 953 final}

1

CONTENTS

1. INTRODUCTION ....................................................................................................... 2

2. OVERALL COMPETITIVENESS OF THE EU CLEAN ENERGY

SECTOR ...................................................................................................................... 4

2.1 Energy and resource trends ................................................................................... 4

2.2 Share of EU energy sector in EU GDP ................................................................. 6

2.3 Human capital ........................................................................................................ 6

2.4 Research and innovation trends ............................................................................. 9

2.5 Covid-19 Recovery .............................................................................................. 11

3. FOCUS ON KEY CLEAN ENERGY TECHNOLOGIES AND

SOLUTIONS ............................................................................................................. 12

3.1 Offshore renewables – wind ................................................................................ 12

3.2 Offshore renewables – Ocean energy .................................................................. 16

3.3 Solar photovoltaics (PV) ..................................................................................... 18

3.4 Renewable hydrogen production through electrolysis ........................................ 20

3.5 Batteries ............................................................................................................... 23

3.6 Smart electricity grids ......................................................................................... 26

3.7 Further findings on other clean and low carbon energy technologies and

solutions ........................................................................................................... 30

CONCLUSIONS ............................................................................................................... 31

2

1. INTRODUCTION

The goal of the European Green Deal

1

, Europe’s new growth strategy, is to transform the

European Union (EU)

2

into a modern, resource-efficient and competitive economy,

which is climate neutral by 2050. The EU’s economy will need to become sustainable,

while making the transition just and inclusive for everyone. The Commission’s recent

proposal

3

to cut greenhouse gas emissions by at least 55% by 2030 sets Europe on that

responsible path. Today, energy production and use account for more than 75% of the

EU’s greenhouse gas emissions. The delivery of the EU’s climate goals will require us to

rethink our policies for clean energy supply across the economy. For the energy system,

this means a steep decarbonisation and an integrated energy system largely based on

renewable energy. By 2030 already, the EU renewable electricity production is set to at

least double from today’s levels of 32% to around 65% or more

4

and by 2050, more than

80% of electricity will be coming from renewable energy sources

5

.

Achieving these 2030 and 2050 targets requires a major transformation of the energy

system. This however depends heavily on uptake of new clean technologies and

increased investments in the needed solutions and infrastructure. However, as well as the

business models, skills, and changes in behaviour to develop and use them. Industry lies

at the heart of this social and economic change. The New Industrial Strategy for Europe

6

gives European industry a central role in the twin green and digital transitions.

Considering the EU’s large domestic market, accelerating the transition will help

modernise the whole EU economy and increasing the opportunities for the EU’s global

clean technologies leadership.

This first annual progress report on competitiveness

7

aims to assess the state of the clean

energy technologies and the EU clean energy industry’s competitiveness to see if their

development is on track to deliver the green transition and the EU’s long-term climate

goals. This competitiveness assessment is also particularly crucial for the economic

recovery from the COVID-19 pandemic, as outlined in the ‘Next Generation EU’

communication

8

. Improved competitiveness has the potential to mitigate the short- and

medium-term economic and social impact of the crisis, while also addressing the longer-

term challenge of the green and digital transitions in a socially fair manner. Both in the

context of the crisis, but also in the long run, improved competitiveness can address

energy poverty concerns, reducing the cost of energy production and the cost of energy

efficiency investments

9

.

It is possible to ascertain the clean energy technology needs for achieving the 2030 and

2050 targets on the basis of the impact assessment referred to in the European

1

COM(2019) 640 final.

2

For the purpose of this report, EU is to be understood as EU27 (i.e. without the UK). Whenever the UK is included,

this report will refer to EU28.

3

COM(2020) 562 final.

4

COM(2020) 562 final.

5

COM/2018/773 final.

6

COM (2020) 102 final.

7

Drawn up in accordance with the requirements of Article 35 (m) of Regulation (EU) 2018/1999

(Governance Regulation)

8

COM(2020) 456 final

9

See also A Renovation Wave for Europe – greening our buildings, creating jobs, improving lives COM(2020)662

accompanied by SWD(2020)550, and Energy Poverty Recommendation C(2020)9600

3

Commission’s Climate Target Plan scenarios

10

. In particular, the EU is expected to invest

in renewable electricity, notably offshore energy (in particular wind) and solar

energy

11

,

12

. This large increase in the share of variable renewables also implies an

increase in storage

13

and in the ability to use electricity in transport and industry,

especially through batteries and hydrogen, and requires major investments in smart grid

technologies

14

. On this basis, the present report focuses on the six technologies

mentioned above

15

, most of which are at the heart of the EU flagship initiatives

16

,

17

aimed

at fostering reforms and investments to support a robust recovery based on twin green

and digital transition. The remaining clean and low-carbon energy technologies included

in the scenarios are analysed in the staff working document with the title ‘Clean Energy

Transition – Technologies and Innovations Report’ (CETTIR) that accompanies this

report

18

.

For the purpose of this report, competitiveness in the clean energy sector

19

is defined as

the capacity to produce and use affordable, reliable and accessible clean energy through

clean energy technologies, and compete in energy technology markets, with the overall

aim of bringing benefits to the EU economy and people.

Competitiveness cannot be captured by a single indicator

20

. Therefore, this report

proposes a set of widely accepted indicators that may be used for this purpose (see table

1 below) capturing the entire energy system (generation, transmission and consumption)

and analysed at three levels (technology, value chain and global market).

10

At time horizon 2050, the 1.5 TECH from the EU 2050 Long Term Strategy (COM (2018) 773) and the Climate

Target plan (COM(2020) 562 final) scenarios display no significant differences and are therefore both referred to

in this report. The CTP MIX scenario achieves around 55% GHG reductions, both expanding carbon pricing and

moderately increasing the ambition of policies.

11

ASSET Study commissioned by DG ENERGY - Energy Outlook Analysis (Draft, 2020) covering LTS 1.5 Life and

Tech, BNEF NEO, GP ER, IEA SDS, IRENA GET TES, JRC GECO 2C_M

12

Tsiropoulos I., Nijs W., Tarvydas D., Ruiz Castello P., Towards net-zero emissions in the EU energy system by 2050

– Insights from scenarios in line with the 2030 and 2050 ambitions of the European Green Deal, JRC118592

13

Study on energy storage - Contribution to the security of the electricity supply in Europe (2020): :

https://op.europa.eu/en/publication-detail/-/publication/a6eba083-932e-11ea-aac4-01aa75ed71a1

14

Between EUR 71 and 110 billion/year of power grid investments between 2031 and 2050 under the different

scenarios, ‘In-depth analysis in support of COM(2018) 773’, table 10, p. 202.

15

Offshore renewables (wind and ocean), solar photovoltaics, renewable hydrogen, batteries and grid technologies.

This selection does not neglect the role of established renewables, in particular bioenergy and hydropower, within

the EU portfolio of low-carbon energy technologies. These are covered in the CETTIR and may be covered in

forthcoming annual reports on progress in competitiveness.

16

European flagship initiatives have been presented in the latest Annual Sustainable Growth Strategy 2021

(COM(2020) 575 final) – section iv.

17

Recent and upcoming initiatives include the upcoming offshore energy strategy and the hydrogen strategy

(COM(2020) 301 final), including the Hydrogen Alliance, the European Batteries Alliance, and the energy system

integration strategy (COM(2020) 299 final). These technologies are also described in a range of national energy

and climate plans.

18

SWD(2020)953 – This includes buildings (incl. heating and cooling); CCS; citizens and communities engagement;

geothermal; high voltage direct current and power electronics; hydropower; industrial heat recovery; nuclear;

onshore wind; renewable fuels; smart cities and communities; smart grids – digital infrastructure; solar thermal

power.

19

In this report and in the SWD, clean energy is considered as all energy technologies included in the EU Long-Term

Strategy to achieve climate neutrality in 2050.

20

Based on the conclusions of the Competitiveness Council (28.07.20).

4

Table 1 Grid of indicators to monitor progress in competitiveness

Competitiveness of EU clean energy industry

1. Technology analysis

Current situation and

outlook

2. Value chain analysis of the

energy technology sector

3. Global market analysis

Capacity installed,

generation

(today and in 2050)

Turnover

Trade (imports, exports)

Cost / Levelised cost of

energy (LCoE)

(today and in 2050)

Gross value added growth

Annual, % change

Global market leaders vs. EU

market leaders

(market share)

Public R&I funding

Number of companies in the

supply chain, incl. EU market

leaders

Resource efficiency and

dependence

Private R&I funding

Employment

Real Unit Energy Cost

Patenting trends

Energy intensity / labour

productivity

Level of scientific

Publications

Community Production

21

Annual production values

Analysis of competitiveness of the clean energy sector can be further developed and

deepened over time, and future competitiveness reports may focus on different angles.

For example by looking in more detail at policies and instruments to support R&I and

competitiveness at the Member State level, how these contribute to the Energy Union and

the Green Deal objectives, looking at competitiveness at subsector

22

, national or regional

level, or by analysing the synergies and trade-offs with environmental or social impacts,

in line with the European Green Deal objectives.

Given the lack of data for a wide range of competitiveness indicators

23

,

24

, some

approximations of a more indirect nature are used (e.g. the level of investment). The

Commission calls on Member States and stakeholders to work together in the context of

the National Energy and Climate Plans (NECPs)

25

and the Strategic Energy Technology

plan to continue developing a common approach to assessing and boosting the

competitiveness of the Energy Union. This is also important for the national recovery and

resilience plans that will be prepared under the Recovery and Resilience Facility.

2. OVERALL COMPETITIVENESS OF THE EU CLEAN ENERGY SECTOR

2.1 Energy and resource trends

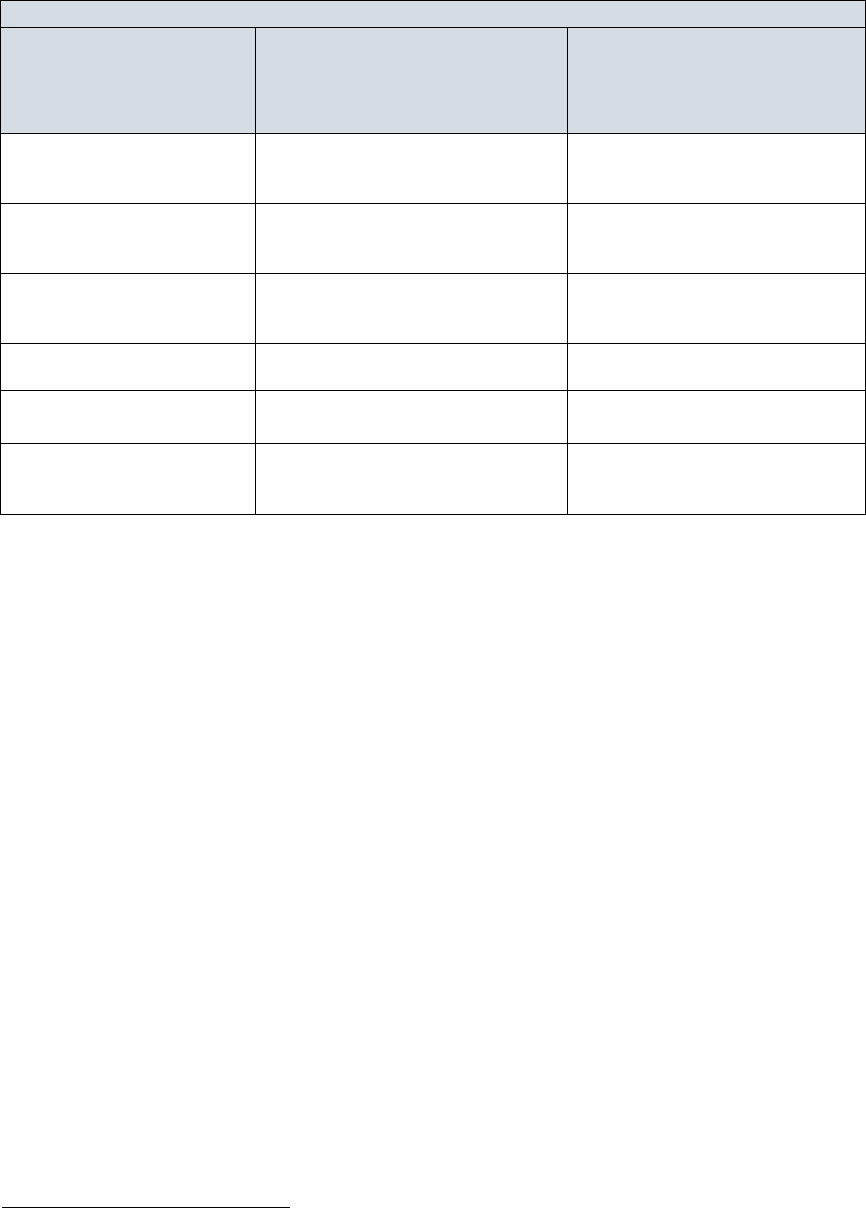

Over 2005-2018, primary energy intensity in the EU decreased at an average annual rate

of nearly 2%, demonstrating the decoupling of energy demand from economic growth.

Final energy intensity in industry and construction followed the same trend, albeit at a

21

This abbreviation means Production Communautaire (PRODCOM dataset).

22

Eg. the scope and role of alternative business models, as well as the role of SMEs and local actors.

23

For an overall mapping of competitiveness definitions, refer to JRC116838, Asensio Bermejo, J.M., Georgakaki, A,

Competitiveness indicators for the low-carbon energy industries - definitions, indices and data sources, 2020.

24

For an overview of missing data, see CETTIR (SWD(2020)953) chapter 5

25

This report builds on and complements the assessment and country-specific guidance of the NECPs (COM/2020/564

final), which include the topic of ‘research, innovation and competitiveness’.

5

slightly slower annual average rate of 1.8%, reflecting the sector’s efforts to reduce its

energy footprint. Enabled by energy policy, the share of renewable energy in final energy

consumption rose from 10% towards the 2020 target of 20%. The share of renewable

energy in the electricity sector rose to just over 32%. It increased to just over 21% in the

heating and cooling sector, while the figure for the transport sector was slightly over 8%.

This shows that the energy system has been shifting gradually towards clean energy

technologies (see Figure 1).

Figure 1 EU primary energy intensity, final energy intensity in industry, renewable energy share

and targets, and net import dependency (fossil fuels)

26

Source 1 EUROSTAT

During the last decade, industrial electricity prices in the EU

27

have remained relatively

stable, and are currently lower than Japan’s, but double those of the US and higher than

those of most non-EU G20 countries. Though industrial gas prices

28

have fallen, and are

lower than those in Japan, China and Korea, they remain higher than those of most non-

EU G20 countries. Relatively high non-recoverable taxes and levies in the EU and price

regulation and/or subsidies in the non-EU G20 play an important role in this difference.

Despite a short-term improvement and reduction in energy import dependency between

2008 and 2013, the EU has since experienced an increase

29

. In 2018, net import

dependency was 58.2%, just over the 2005 level, and almost equalling the highest values

over the period. Resource efficiency and economic resilience are key in being

competitive and enhancing the open strategic autonomy

30

of the EU in the clean energy

technology market. While clean energy technologies reduce dependence on imports of

fossil fuels, they risk replacing this dependence with on raw materials. This creates a new

type of supply risk

31

. However, unlike fossil fuels, raw materials have the potential to

stay in the economy through the implementation of circular economy approaches

32

, like

extended value chains, recycling, reuse and design for circularity, affecting the capital

expenditures and decreasing the energy need for extraction and processing of virgin

materials but not the operational expenditures of energy production. The EU is very

dependent on third countries for raw and processed materials. For some technologies,

however, it has a leading position in the manufacture of components and final products,

26

Energy Union indicators EE1-A1, EE3, DE5-RES, and SoS1.

27

EU weighted average (see COM(2020)951).

28

EU weighted average (see COM(2020)951).

29

Plausible reasons include the exhaustion of EU gas sources, weather variability, the economic crises and fuel shift.

30

COM(2020) 562 final.

31

COM(2020) 474 final and Critical Raw Materials for Strategic Technologies and Sectors in the EU - A Foresight

Study, https://ec.europa.eu/docsroom/documents/42882

32

The Circular Economy Action Plan puts in focus the creation of a secondary raw material market and design for

circularity (COM/2015/0614 final and COM/2020/98 final)

6

or high technology components. Specific, often high-tech materials show high supply

concentration in a handful of countries. (For instance, China produces over 80% of the

available rare earths for permanent magnet generators)

33

.

2.2 Share of EU energy sector in EU GDP

The turnover of the EU energy sector

34

was EUR 1.8 trillion in 2018, nearly the same

level as in 2011 (EUR 1.9 trillion). The sector contributes 2% of total gross value added

in the economy, a figure that has remained largely constant since 2011. The turnover of

the fossil fuel sector shrank from 36% (EUR 702 billion) of the overall energy sector

turnover in 2011 to 26% (EUR 475 billion) in 2018. At the same time, the turnover from

renewables increased over the same period from EUR 127 billion to EUR 146 billion

35

,

36

.

The value added of the clean energy sector (EUR 112 billion in 2017) was more than

double that of fossil fuel extraction and manufacturing activities (EUR 53 billion), having

tripled since 2000. The clean energy sector thus generates more value added that stays

within Europe than the fossil fuel sector.

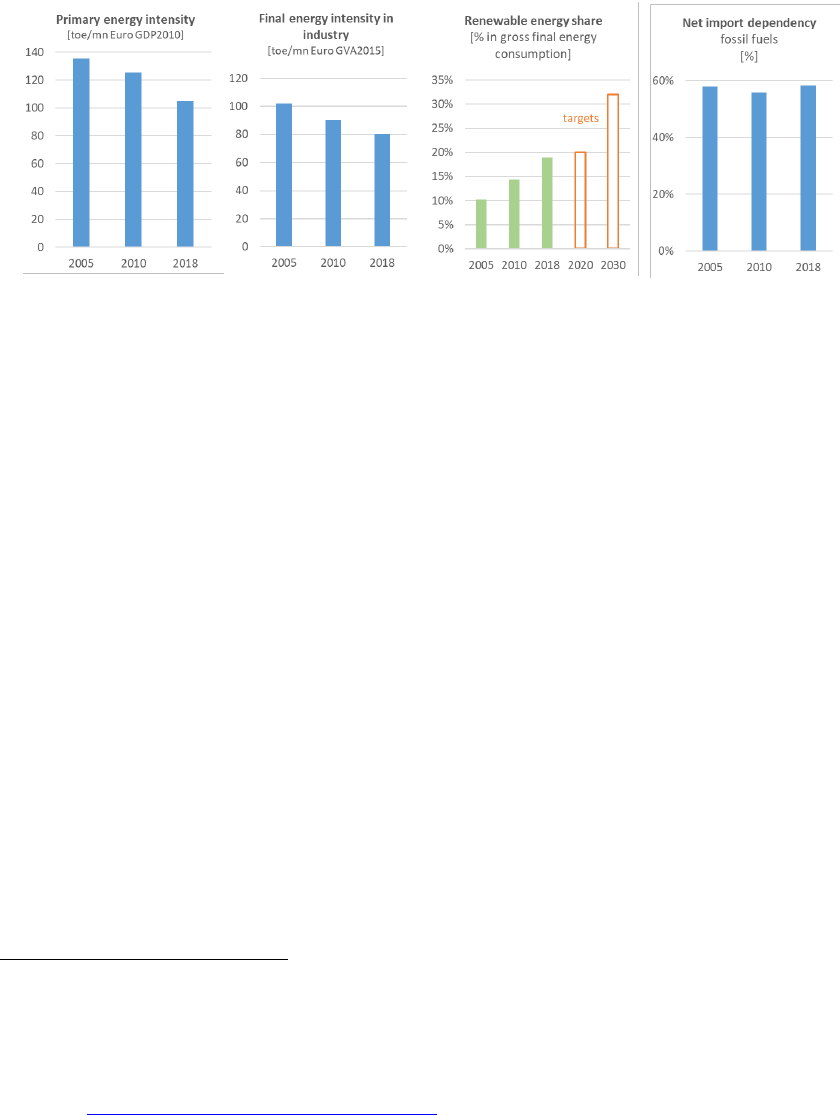

Over 2000-2017, annual growth in the gross value added of renewable energy production

averaged 9.4%, while that of energy efficiency activities averaged 22.3%, far outpacing

the rest of the economy (1.6%). The labour productivity of the EU (gross value added per

employee) has also improved significantly in the clean energy sector, especially in the

renewable energy production sector, where it has risen by 70% since 2000.

Figure 2 Gross value added and value added per employee, 2000-2019, 2000=100

Source 2 JRC based on Eurostat data: [env_ac_egss1], [nama_10_a10_e], [env_ac_egss2],

[nama_10_gdp.

2.3 Human capital

Clean energy technologies and solutions provide direct full-time employment for 1.5

million people in Europe

37

, of which more than half million

38

in renewables (growing to

33

D. T. Blagoeva, P. Alves Dias, A. Marmier, C.C. Pavel (2016) Assessment of potential bottlenecks along the

materials supply chain for the future deployment of low-carbon energy and transport technologies in the EU.

Wind power, photovoltaic and electric vehicles technologies, time frame: 2015-2030; EUR 28192 EN;

doi:10.2790/08169

34

This is based on Eurostat’s Structural Business Statistics Survey. The following codes are included: B05 (mining of

coal and lignite), B06 (extraction of crude petroleum and natural gas), B07.21 (mining uranium and thorium ores),

B08.92 (extraction of peat), B09.1 (support activities for petroleum and natural gas extraction), C19 (manufacture

of coke and refined petroleum products), and D35 (electricity, gas, steam and air conditioning supply).

35

Eurostat [sbs_na_ind_r2]

36

EurObserv'ER

37

To give some perspective, direct employment in fossil fuel extraction and manufacturing (NACE B05, B06, B08.92,

B09.1, C19) was 328,000 in the EU27 in 2018, while it was 1.2 million in the electricity, gas, steam and air

7

1.5 million when indirect jobs are also included) and almost 1 million in energy

efficiency activities (in 2017)

39

. Direct jobs in renewable energy production for the EU

grew from 327,000 in 2000 to 861,000 in 2011, falling to 502,000 in 2017. As Figure 3

shows, there was a decrease after 2011

40

, probably explained by the effect of the

financial crisis, including the subsequent relocation of manufacturing capacity, as well as

by increased productivity and a decrease in job intensity. The number of direct jobs in

energy efficiency increased steadily from 244,000 in 2000 to 964,000 in 2017. Direct

jobs in these sectors (RES and EE) represent about 0.7% of total employment in EU,

41

but their growth has outpaced the rest of the economy, with average annual growth of

3.1% and 17.4% respectively

42

.

conditioning sector (NACE D35), which supplies electricity from both renewable and fossil energy sources. The

total figure for the broad energy sector has remained largely stable, although employment has fallen by about

80,000 in the mining of coal and lignite and by about 30,000 in the extraction of crude petroleum and natural gas.

See: JRC120302, Employment in the Energy Sector Status Report 2020, EUR 30186 EN, Publications Office of

the European Union, Luxembourg, 2020.

38

If indirect jobs are also taken into account, the renewable energy sector employs nearly 1.4 million people in the

EU27, according to EurObserv'ER. EurObserv'ER includes in its estimate both direct and indirect employment.

Direct employment includes renewable equipment manufacturing, renewable plant construction, engineering and

management, operation and maintenance, biomass supply and exploitation. Indirect employment refers to

secondary activities, such as transport and other services. Induced employment is outside the scope of this

analysis. EurObserv'ER uses a formalised model to assess employment and turnover.

39

Eurostat Environmental Goods and Services Sector (EGSS) data is estimated by combining data from different

sources (SBS, PRODCOM, National Accounts). In EGSS, information is reported on the production of goods and

services that have been specifically designed and produced for the purpose of environmental protection or

resource management. The unit of analysis in EGSS is the establishment. The establishment is an enterprise or

part of an enterprise that is situated in a single location and in which a single activity is carried out or in which the

principal productive activity accounts for most of the value added. It is also tracked across all NACE codes. We

use CREMA 13A Production of energy from renewable sources and CREMA 13B for Heat/energy saving and

management.

40

This decrease can probably be explained by the effect of the financial crisis, including the subsequent relocation of

manufacturing capacity, as well as by increased productivity and a decrease in job intensity (Sources: JRC120302

Employment in the Energy Sector Status Report, 2020). The decrease was led by solar PV and by geothermal

energy to a lesser extent. The effect of the crisis was seen in the drop in solar PV installations and relocation of

manufacturing to Asia. For the onshore and offshore wind energy sector, increased productivity and thus

decreased job intensity can be particularly observed. Comparing direct employment with the cumulative installed

capacity in the last decade unveils a decrease of 47% and 59% in specific employment for the onshore and

offshore wind sector, respectively (sources: GWEC 2020, Global Offshore Wind Report, 2020; WindEurope

2020, Update of employment figures based on WindEurope, Local Impact Gl). Based on EurObserv’ER, job

intensity (jobs/MW) fell by 19% in wind and by 14% in solar PV over 2015-2018. Dynamics in the energy

efficiency sector are different (e.g. energy saving and efficiency has a direct positive impact through reduced

costs), and the growth in EE jobs can partially be explained by strong growth of jobs in the heat pump sector since

2012 (EurObservER). Overall, we can see from EurObserv’ER, which accounts for direct and indirect jobs, an

increasing trend for RES employment in the EU27.

41

Eurostat, EGSS.

42

In the rest of the economy, average annual growth has been 0.5%.

8

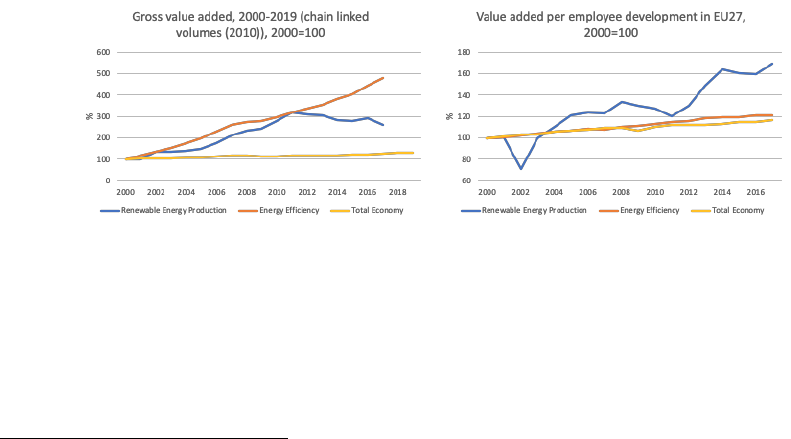

Figure 3 Direct employment in the clean energy sector vs the rest of the economy over 2000-

2018, 2000=100, and Renewable energy employment per technology, 2015-2018

Source 3 (JRC based on Eurostat data [env_ac_egss1], [nama_10_a10_e]

43

and

EurObserv'ER)

The growing trend of employment in the clean energy sector is global, although the

technologies that offer more employment opportunities vary by region. In general, jobs

have been created mainly in the solar PV and wind energy sectors. China, which has

almost 40% of all global jobs in renewables, employs most in solar PV, solar heating and

cooling, and wind energy; Brazil’s employment is in the bioenergy sector; and the EU

employ most people in bioenergy (about half of all RES jobs) and wind energy (about a

quarter), see Figure 4.

Figure 4 Global employment in renewable energy technology (2012-2018)

44

Source 4 (JRC based on IRENA, 2019

45

)

The clean energy technology sector continues to face challenges, in particular availability

of skilled workers at the locations where they are in demand.

46

,

47

The skills concerned

include, in particular, engineering and technical skills, IT literacy and ability to utilise

new digital technologies, knowledge of health and safety aspects, specialised skills in

carrying out work in extreme physical locations (for example at height or at depth), and

soft skills like team work and communication, as well as knowledge of the English

language.

As regards gender, women accounted for an average of 32% of the workforce in the

renewables sector in 2019

48

. This figure is higher than in the traditional energy sector

43

Renewable energy production refers to Eurostat EGSS code CREMA13A and energy efficiency activities to

CREMA13B.

44

The employment figures per country are for 2017.

45

IRENA. 2019. Renewable Energy and Jobs – Annual Review 2019.

46

Strategy baseline to bridge the skills gap between training offers and industry demands of the Maritime Technologies

value chain, September 2019 - MATES Project. https://www.projectmates.eu/wp-

content/uploads/2019/07/MATES-Strategy-Report-September-2019.pdf

47

Alves Dias et al. 2018. EU coal regions: opportunities and challenges ahead. https://ec.europa.eu/jrc/en/publi

cation/eur-scientific-and-technical-research-reports/eu-coal-regions-opportunities-and-challenges-ahead.

48

IRENA 2019: https://www.irena.org/publications/2019/Jan/Renewable-Energy-A-Gender-Perspective

9

(25%

49

) but lower than the share across the economy (46.1%

50

) and furthermore gender

balance differs to a higher extend for certain job profiles.

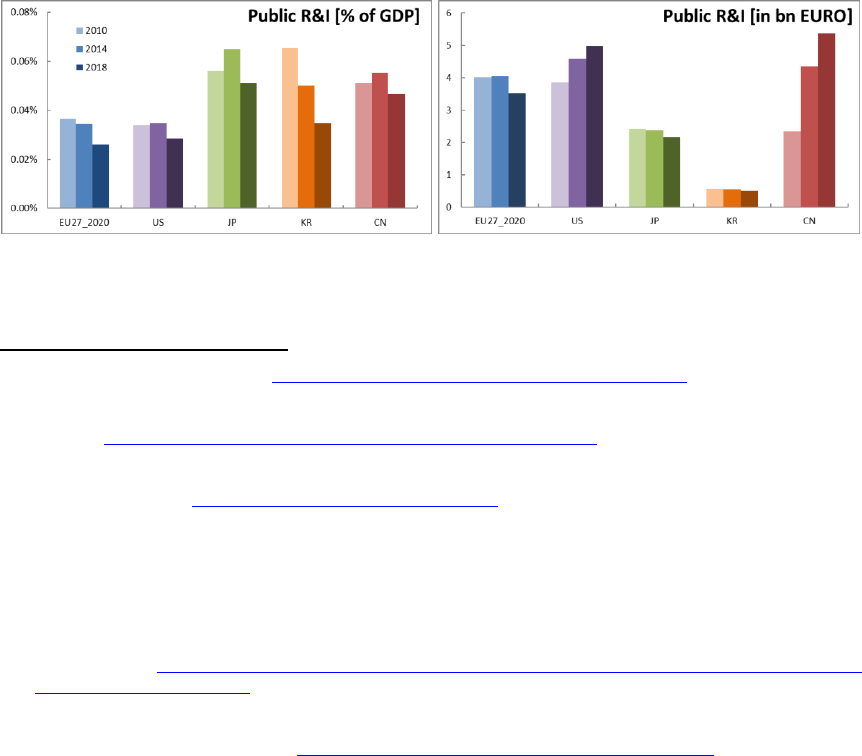

2.4 Research and innovation trends

In recent years, the EU has invested an average of nearly EUR 20 billion a year on clean

energy R&I prioritised by the Energy Union

51

,

52

. EU funds contribute 6%, public funding

from national governments accounts for 17%, and business contributes an estimated

77%.

The R&I budget allocated to energy in the EU represents 4.7% of total spending on

R&I

53

. In absolute terms, however, Member States have reduced their national R&I

budgets for clean energy (Figure 5); in 2018 the EU spent half a billion less than in 2010.

This trend is global. Public sector R&I spending on low-carbon energy technologies was

lower in 2019 than in 2012, while countries continue to allocate large amounts of R&I

funding to fossil fuels

54

. This is the opposite of what is needed: R&I investments in clean

technologies need to increase if the EU and the world want to meet their decarbonisation

commitments. Today the EU has the lowest investment rate of all major global

economies measured as a share of GDP (Figure 5). EU research funds have been

contributing a larger share of public funding and have been essential in maintaining

research and innovation investment levels over the last four years.

Figure 5 Public R&I financing of Energy Union R&I priorities

55

Source 5 JRC

49

based on IEA

56

, MI

57

.

49

Eurostat (2019), retrieved from https://ec.europa.eu/eurostat/web/equality/overview

50

Eurostat [lfsa_egan2], 2019.

51

COM(2015)80; renewables, smart system, efficient systems, sustainable transport, CCUS and nuclear safety.

52

JRC SETIS https://setis.ec.europa.eu/publications/setis-research-innovation-data;

JRC112127 Pasimeni, F.; Fiorini, A.; Georgakaki, A.; Marmier, A.; Jimenez Navarro, J. P.; Asensio Bermejo, J.

M. (2018): SETIS Research & Innovation country dashboards. European Commission, Joint Research Centre

(JRC) [Dataset] PID: http://data.europa.eu/89h/jrc-10115-10001, according to:

JRC Fiorini, A., Georgakaki, A., Pasimeni, F. and Tzimas, E., Monitoring R&I in Low-Carbon Energy Technologies,

EUR 28446 EN, Publications Office of the European Union, Luxembourg, 2017.

JRC117092 Pasimeni, F., Letout, S., Fiorini, A., Georgakaki, A., Monitoring R&I in Low-Carbon Energy

Technologies, Revised methodology and additional indicators, 2020 (forthcoming).

53

Eurostat, Total GBAORD by NABS 2007 socio-economic objectives [gba_nabsfin07]. The energy socioeconomic

objective includes R&I in the field of conventional energy. The Energy Union R&I priorities would also fall under

other socioeconomic objectives.

54

IEA ETP https://www.iea.org/reports/clean-energy-innovation/global-status-of-clean-energy-innovation-in-

2020#government-rd-funding

55

Excludes EU funds.

56

Adapted from the 2020 edition of the IEA energy technology RD&D budgets database.

57

Mission Innovation Tracking Progress http://mission-innovation.net/our-work/tracking-progress/

10

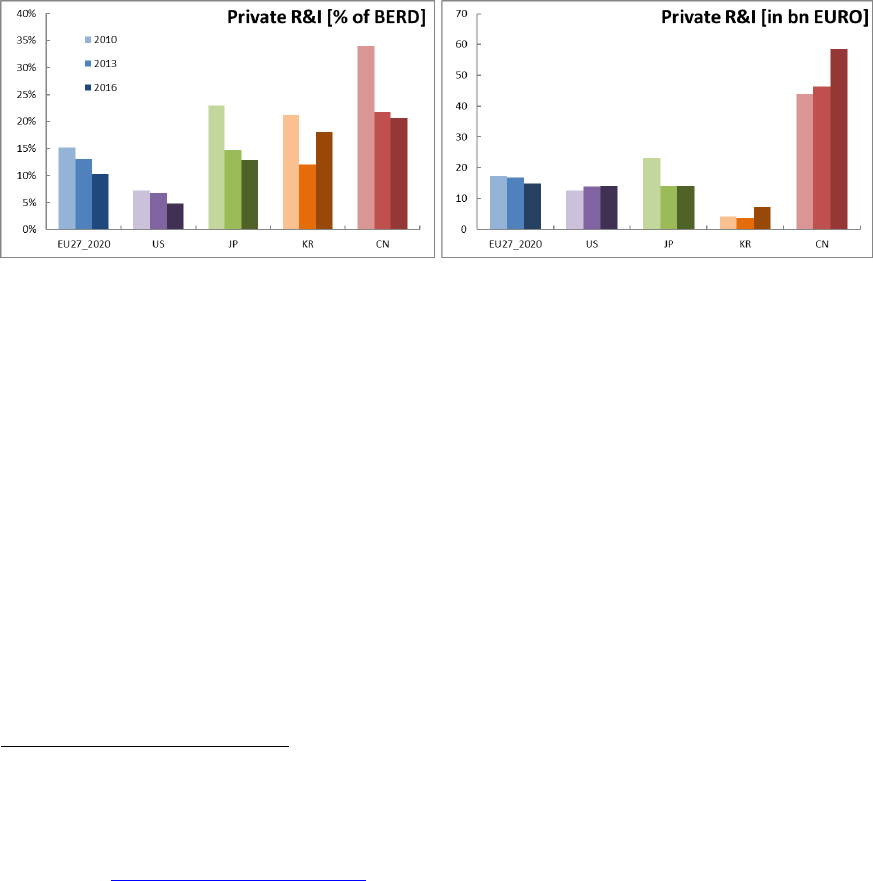

In the private sector, only a small share of revenue is currently being spent on R&I in the

sectors most in need of large-scale adoption of low-carbon technologies

51

. The EU have

estimated that private investment in Energy Union R&I priorities has been decreasing: it

currently amounts to around 10% of businesses’ total expenditure on R&I

58

. This is

higher than the US and comparable to Japan, but lower than China and Korea. A third of

this investment goes on sustainable transport, while renewables, smart systems and

energy efficiency receive about a fifth each. While the distribution of private R&I in the

EU has changed only slightly in recent years, there has been a more significant shift

globally towards industrial energy efficiency and smart consumer technologies

59

.

Figure 6 Estimates of private R&I financing of Energy Union R&I priorities

60

Source 6 JRC

49

, Eurostat/OECD

55

On average, major listed companies and their subsidiaries make up 20-25% of the main

investors, but account for 60-70% of patenting activity and investments. In the EU, the

automotive sector is the biggest private R&I investor in absolute terms in the Energy

Union R&I priorities

61

, followed by biotechnology and pharmaceuticals. Figure 7 shows

that among the energy industries, the oil and gas sector is the largest investor in R&I.

Other energy sectors, such as electricity or alternative energy companies, have much

lower budgets for R&I, although they spend more of it on clean energy. It is worrying

that a major share of the private budget for R&I in the energy sector is not spent on clean

energy technologies. According to the IEA, less than 1% of oil and gas companies’ total

capital expenditure has been outside their core business areas, on average

62

,

63

, and only

8% of their patents are in clean energy

64

.

Figure 7 EU R&I investment in Energy Union R&I priorities, by industrial sector

65

58

Contrasted with BERD statistics: Eurostat/OECD business expenditure on R&D (BERD) by NACE Rev. 2 activity

and source of funds [rd_e_berdfundr2]; The utilities sector includes water collection, treatment and supply

services; data not available for all countries.

59

JRC118288 input to Mission Innovation (2019) ‘Mission Innovation Beyond 2020: challenges and opportunities’.

60

Estimates for China are particularly challenging and uncertain, given differences in intellectual property protection

(see also https://chinapower.csis.org/patents/), and the difficulties faced in mapping company structures (e.g.

state-backed companies) and financial reporting.

61

This is a wider definition of what clean energy technology includes than that used in this report. For example, this

broader definition includes R&I in energy efficiency in industry.

62

With some leading individual companies spending around 5% on clean energy.

63

The oil and gas industry in energy transitions, world energy outlook special report, IEA, January 2020,

https://www.iea.org/reports/the-oil-and-gas-industry-in-energy-transitions

64

The Energy Transition and Oil Companies’ Hard Choices – Oxford Institute for Energy Studies, July 2019; Rob

West, Founder, Thundersaid Energy & Research Associate, OIES and Bassam Fattouh, Director, OIES, page 4.

65

Top contributing sectors. Five-year average (2012-2016) per sector; a third of companies (non-listed, smaller

investors) cannot be allocated to a specific sector.

11

Source 7 JRC

49

Venture capital (VC) investment in clean energy had been increasing in recent years, but

remains low (just over 6-7%) compared with private-sector investment in R&I. So far,

2020 marks a significant global slowdown in VC investment in clean energy

technologies

66

.

Patenting activity in clean energy technologies

67

peaked in 2012, and has been in decline

since.

68

Within this trend, however, certain technologies that are increasingly important

for the clean energy transition (e.g. batteries) have maintained or even increased their

levels of patenting activity.

The EU and Japan lead among international competitors in high-value

69

patents on clean

energy technologies. Clean energy patents account for 6% of all high-value inventions in

the EU. The EU’s share is similar to that of Japan, and higher than China (4%), the US

and the rest of the world (5%), and second only to Korea (7%) in terms of competing

economies. The EU host a quarter of the top 100 companies in terms of high-value

patents in clean energy. The majority of inventions funded by multinational firms

headquartered in the EU are produced in Europe and, for the most part, by subsidiaries

located in the same country.

70

The US and China are the main IPO offices – and by

extension markets – targeted for protection of EU inventions.

2.5 Covid-19 Recovery

71

During the pandemic, the European energy system has proved to be resilient to shocks

stemming from the pandemic

72

and a greener energy mix has emerged, with coal power

generation in the EU falling by 34% and renewables providing 43% of power generation

66

JRC

52

and JRC analysis based on Pitchbook, and IEA data on CleanTech VC investments.

67

Low-carbon energy technologies under the Energy Union’s R&I priorities.

68

With the exception of China, where local applications keep increasing, without seeking international protection. (See

also: Are Patents Indicative of Chinese Innovation? https://chinapower.csis.org/patents/)

69

High-value patent families (inventions) are those containing applications to more than one office i.e. those seeking

protection in more than one country / market.

70

Incentives, language and geographical proximity explain major exceptions.

71

Based on JRC work on the impacts of Covid-19 on the energy system and value chain.s

72

SWD(2020) 104 - Energy security: good practices to address pandemic risks

12

in Q2 2020, the highest share to date

73

. At the same time, the stock market performance

of the clean energy sector has seemed less affected and recovered more quickly than

fossil-fuel sectors. Digitalisation has helped companies and sectors respond successfully

to the crisis, also boosting the emergence of new digital applications.

Although the EU energy value chains are recovering, the crisis has brought to the

forefront the question of optimising and potentially regionalising supply chains, to reduce

exposure to future disruptions and improve resilience. In response, the Commission aims

to identify the critical supply chains for energy technologies, analyse potential

vulnerabilities and improve their resilience

74

. The key energy priorities in recovery are

energy efficiency in particular through the renovation wave, renewable energy sources,

hydrogen and energy system integration. There is a further concern that the pandemic is

affecting investments in and resources available for R&I, as has demonstrably happened

in previous economic crises.

Recovery measures can take advantage of the job creation potential offered by energy

efficiency and renewable energy

75

, including that of the R&I sector, to boost employment

while also moving towards sustainability. Support for R&I investment, including

corporate R&I, has a greater positive impact on employment in medium- to high-

technology sectors such as cleaner energy technology

76

. At the same time, breakthrough

low-carbon technologies are needed, for instance in energy-intensive industries, which

will require faster R&I investment for their demonstration and deployment.

3. FOCUS ON KEY CLEAN ENERGY TECHNOLOGIES AND SOLUTIONS

In the section below, the most relevant competitiveness values for each of the six

technologies analysed above, and the status, value chain and global market are analysed,

based on the indicators outlined in Table 1. The EU's performance is compared as far as

possible with other key regions (e.g. USA, Asia). A more detailed assessment of other

important clean and low carbon energy technologies needed to reach climate neutrality is

set out in the accompanying Clean Energy Transition – Technologies and Innovation

Report

77

.

3.1 Offshore renewables – wind

Technology: the EU cumulative installed capacity of offshore wind (OW) amounted to

12 GW in 2019

78

. At the 2050 time horizon, EU scenarios foresee approximately 300

GW of wind offshore capacity in the EU

79

. Globally, costs have fallen steeply in recent

years, and demand has been stimulated by new tenders implemented worldwide and the

building of subsidy-free wind parks. OW has benefited considerably from onshore wind

developments, especially economies of scale (e.g. material developments and common

73

Quarterly Report on European Electricity Markets, Volume 13, Issue 2. https://ec.europa.eu/energy/data-

analysis/market-analysis_en?redir=1

74

The analysis is supported by a study planned to deliver its conclusions in April 2021.

75

It is estimated that the same level of spending will generate nearly three times as many jobs as in fossil-fuelled

industries Source: Heidi Garrett-Peltier, Green versus brown: Comparing the employment impacts of energy

efficiency, renewable energy, and fossil fuels using an input-output model, Economic Modelling, Volume 61, 2017,

439-447

76

EC work for MI Tracking Progress: The Economic Impacts of R&D in the Clean Energy Sector and COVID-19,

2020, MI Webinar, May 6, 2020

77

SWD(2020)953

78

GWEC, Global Wind Energy Report 2019 (2020).

79

According to the CTP-MIX scenario from COM(2020) 562 final.

13

components), thereby allowing efforts to focus on the technology’s most innovative

segments (such as floating offshore wind, new materials and components). Recent

offshore wind projects have observed much increased capacity factors. The average

power capacity of the turbines has increased from 3.7 MW (2015) to 6.3 MW (2018),

thanks to sustained R&I efforts.

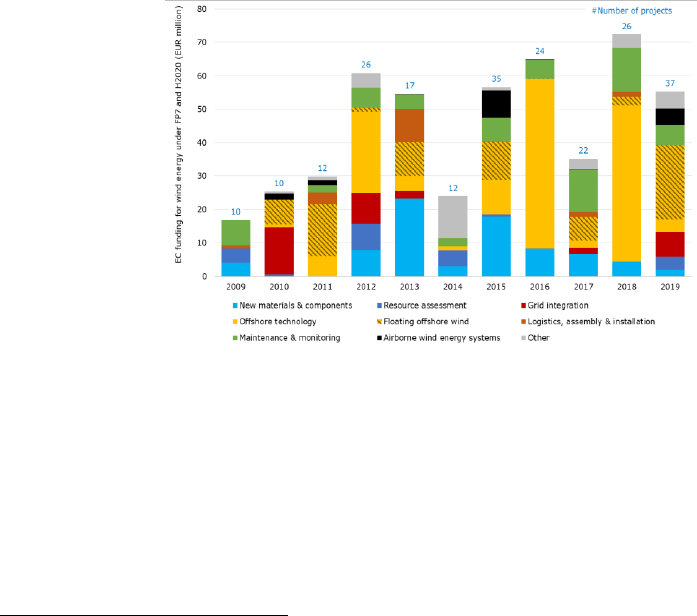

R&I in offshore wind revolves mainly around increased turbine size, floating

applications (particularly substructure design), infrastructure developments, and

digitalisation. About 90% of EU R&I funding for wind comes from the private sector

80

.

At EU level, offshore wind R&I has been supported since the 1990s. Offshore wind, in

particular floating, have received substantial funding in recent years (Figure 8). These

R&I patterns highlight that through the development of new market segments the EU

could establish a competitive edge. For example, a fully-fledged EU OW supply chain

(extended also to untapped EU sea basins), leadership in floating offshore industry

targeting markets with deeper waters or new emerging concepts e.g. airborne wind

systems or the development of a port infrastructure capable to deliver the ambitious

targets (and synergies to other sectors e.g. hydrogen production in ports). Patenting

trends confirm Europe’s competitiveness in wind energy. EU players are leading in high

value inventions

81

and they protect their knowledge in other patent offices outside their

home market.

Figure 8 Evolution of EC R&I funding, categorised by R&I priorities for wind energy under FP7

and H2020 programmes and the number of projects funded over 2009-2019.

Source 8 JRC 2020

82

Other recent innovations target the logistics/supply chain, e.g. the development of wind

turbine gearboxes compact enough to fit into a standard shipping container

83

as well as

applying circular economy approaches along the life-cycle of installations. Further

innovations and trends expected to increase most over the next ten years include

superconducting generators, advanced tower materials and the added value of offshore

wind energy (system value of wind). The SET Plan Group on OW identified most of

80

JRC Technology Market Report – Wind Energy (2019).

81

This means that the patents are protected in other patent offices outside the issuing country and refer to patent

families that include patent applications in more than one patent office. About 60% of all EU wind-related

inventions were protected in other countries (by way of a comparison, only 2% of Chinese inventions were

protected in other patent offices outside China).

82

JRC 2020, Low Carbon Energy Observatory, Wind Energy Technology Development Report 2020, European

Commission, 2020, JRC120709.

83

SET-Plan, Offshore Wind Implementation Plan (2018).

14

these areas as key for Europe to remain competitive in the future. Currently, Europe is

leading in all parts of the value chain of sensing and monitoring systems for OW

turbines, including research and production

84

.

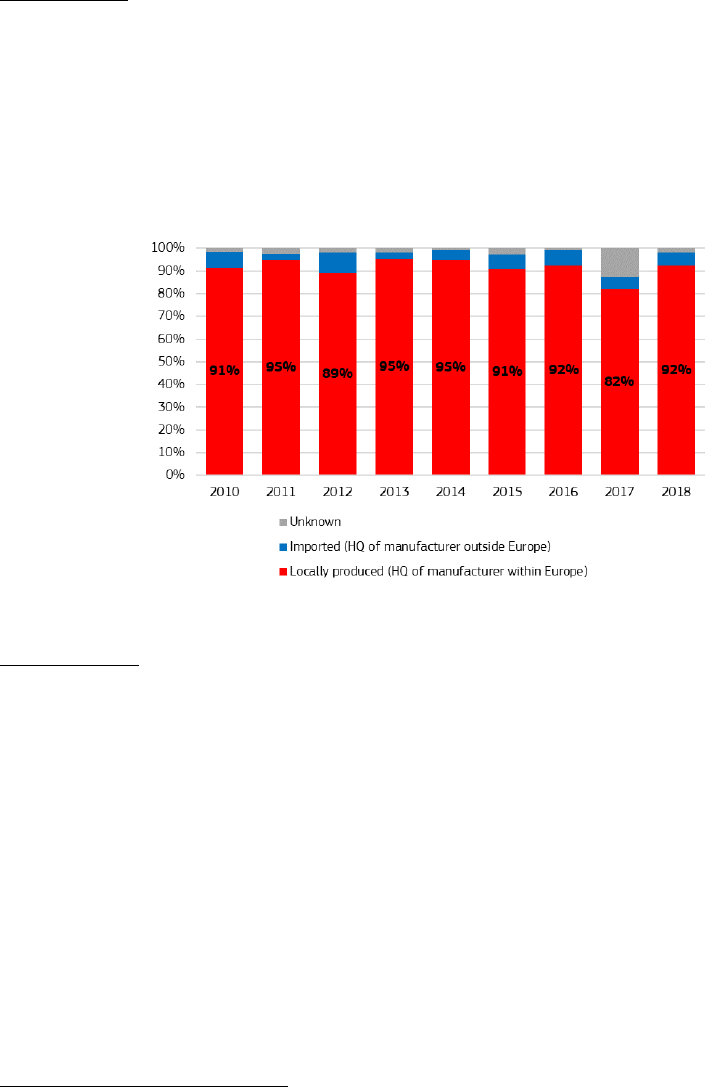

Value chain: On the market side, EU companies are ahead of their competitors in

providing offshore generators of all power ranges, reflecting a well-established European

offshore market and the increasing size of newly installed turbines

85

. Currently, about

93% of the total offshore capacity installed in Europe in 2019 is produced locally by

European manufacturers (Siemens, Gamesa Renewable Energy, MHI Vestas and

Senvion

86

).

Figure 9 Newly installed wind capacity (onshore & offshore) - local vs imported, assuming an

European single market

Source 9 JRC 2020

87

Global market: the EU

88

share of global exports increased from 28% in 2016 to 47% in

2018, and 8 out of the top 10 global exporters were EU countries, with China and India

being the key global competitors. Between 2009 and 2018, the EU

89

trade balance

remained positive, showing a rising trend.

In terms of global markets projections, within Asia (including China), offshore wind

capacity is expected to reach around 95 GW by 2030 (out of a projected global capacity

of almost 233 GW by 2030)

90

. Nearly half of global offshore wind investment in 2018

took place in China

91

. At the same 2030 time horizon, the CTP-MIX scenario projects 73

GW of wind offshore capacity in the EU. Currently, the NECPs project 55 GW of

offshore wind capacity by 2030.

Floating applications seem to become a viable option for EU countries and regions

lacking shallower waters (floating OW farms for depths between 50 and 1000 metres)

and could open up new markets based on areas such as the Atlantic Ocean, the

84

ICF, commissioned by DG Grow – Climate neutral market opportunities and EU competitiveness study (2020)

85

JRC Technology Market Report – Wind Energy (2019).

86

An even stronger market concentration can be expected following the insolvency of Senvion and the closure of its

Bremerhaven turbine manufacturing plant at the end of 2019.

87

JRC 2020, Facts and figures on Offshore Renewable Energy Sources in Europe, JRC121366 (upcoming).

88

EU including UK.

89

EU including UK.

90

GWEC 2020, Global Offshore Wind Report, 2020.

91

IRENA – Future of wind (2019, p. 52).

15

Mediterranean and, potentially, the Black Sea. A number of projects are planned or

underway that will lead to the installation of 350 MW of floating capacity in European

waters by 2024. Moreover, the EU wind industry aims to install floating OW farms with

150 GW of capacity by 2050 in European waters with a view to achieving climate

neutrality

92

. The global market for energy from floating OW farms represents a

considerable commercial opportunity for EU companies. A total of about 6.6 GW from

this source are expected by 2030, with significant capacities in certain Asian countries

(South Korea and Japan), in addition to the European markets (France, Norway, Italy,

Greece, Spain) between 2025 and 2030. Since China has abundant wind resources in

shallow waters, it is not expected to build floating wind farms with significant capacity in

the medium term

93

. Floating applications can also reduce under-water environmental

impacts, notably during the construction phase.

Offshore wind is a competitive industry on the global market. Emerging global market

demands, such as that for energy generated by floating wind farms, may become key to

EU industry if it is to be competitive in the growing offshore wind industry, and remain

so. A key consideration is whether Member States will commit to wind energy. The

current mismatch between the 2030 NECP projection (55 GW of offshore wind) and the

EU’s scenario (73 GW

94

) means that investment must be stepped up. The positive impact

of offshore wind development on supply chains in sea basins is relevant to regional

development (location of manufacturing, assembly of turbines close to the market,

impact on port infrastructure). The offshore renewable energy strategy

95

will define a set

of measures to overcome challenges and boost offshore prospects.

3.2 Offshore renewables – Ocean energy

Technology: tidal and wave energy technologies are the most advanced of the ocean

energy technologies, with significant potential located in a number of Member States and

regions

96

. Tidal technologies can be considered as being at the pre-commercial stage.

Design convergence has helped the technology develop and generate a significant

amount of electricity (over 30 GWh since 2016

97

). A number of projects and prototypes

have been deployed across Europe and worldwide. Most of the wave energy

technological approaches, however, are at technology readiness level (TRL) 6-7, with a

strong focus on R&I. Most improvements in wave energy results stem from ongoing

projects in the EU. Over the past five years, the sector has shown resilience

98

and

significant technology progress has been achieved thanks to the successful deployment of

demonstration and first-of-a-kind farms.

99

The LTS scenarios foresee limited uptake of ocean energy technology. The high cost of

wave and tidal energy converters and the limited information available on the

performance limit the capture of ocean energy in the model

100

. At the same time, the

92

ETIPWind, Floating Offshore Wind. Delivering climate neutrality (2020).

93

GWEC 2020, Global Offshore Wind Report, 2020.

94

The CTP-MIX scenario from COM(2020) 562 final.

95

It is anticipated that this will be published later in 2020.

96

There is significant potential to develop tidal energy in France, Ireland and Spain, and localised potential in other

Member States. As regards wave energy, high potential is to be found in the Atlantic, localised potential in the

North Sea, the Baltic, the Mediterranean, and the Black Sea.

97

Ofgem Renewable Energy Guarantees Origin Register. https://www.renewablesandchp.ofgem.gov.uk/

98

European Commission (2017) Study on Lessons for Ocean Energy Development, EUR 27984.

99

Magagna & Uihllein (2015) 2014 JRC Ocean Energy Status Report.

100

In the years to come, EU energy modelling results can be expected to reflect the validation and cost reduction of

these technologies.

16

European Green Deal emphasises the key role marine renewable energy will play in the

transition to a climate-neutral economy, with a significant contribution expected under

the right market and policy conditions (2.6 GW by 2030

101

and 100 GW in European

waters by 2050

102

). Ongoing demonstrations show that costs can be reduced fast: data

from Horizon 2020 projects indicate that the cost of tidal energy fell by over 40%

between 2015 and 2018

103

,

104

.

Value chain: European leadership spans the whole ocean energy supply chain

105

and

innovation system

106

. The European cluster formed by specialised research institutes,

developers and the availability of research infrastructure has enabled Europe to develop

and maintain its current competitive position.

Global market: the EU maintains global leadership despite the UK’s withdrawal from the

bloc and changes in the market for wave and tidal energy technologies. 70% of global

ocean energy capacity has been developed by EU-based companies

107

. Over the next

decade it will be vital for EU developers to build on their competitiveness position.

Global ocean energy capacity is expected to increase to 3.5 GW within the next five

years, and an increase of up to 10 GW can be expected by 2030

108

.

Figure 10 Installed capacity by origin of technology

Source 10 JRC 2020

109

Within the EU

110

, 838 companies in 26 countries filed patents or were involved in the

filing of patents to do with ocean energy between 2000 and 2015

111

. The EU has long

maintained technological leadership in developing ocean energy technologies, thanks to

101

European Commission (2018) Market study on ocean energy.2.2GW of tidal stream and 423MW of wave energy.

102

European Commission (2017) Ocean energy strategic roadmap: building ocean energy for Europe.

103

JRC (2019) Technology Development Report LCEO: Ocean Energy.

104

In addition, R&I in the fields of advanced and hybrid materials, new manufacturing processes and additive

manufacturing employing innovative 3D technologies could enable costs to be reduced further. It could also help

reduce energy consumption, shorten lead times and improve quality associated with the production of large

cast components.

105

JRC (2017) Supply chain of renewable energy technologies in Europe.

106

JRC (2014) Overview of European innovation activities in marine energy technology.

107

JRC (2020) - Facts and figures on Offshore Renewable Energy Sources in Europe, JRC121366 (upcoming).

108

EURActive (2020) https://www.euractiv.com/section/energy/interview/irena-chief-europe-is-the-frontrunner-on-

tidal-and-wave-energy/

109

JRC (2020) - Facts and figures on Offshore Renewable Energy Sources in Europe, JRC121366 (upcoming).

110

EU including UK.

111

JRC (2020) Technology Development Report Ocean Energy 2020 Update.

17

the sustained support provided for R&I. Between 2007 and 2019, total R&I expenditure

on wave and tidal energy amounted to EUR 3.84 billion, most of which (EUR 2.74

billion) came from private sources. In the same period, national R&I programmes

contributed EUR 463 million to the development of wave and tidal energy, while EU

funds supported R&I to the tune of almost EUR 650 million (including NER300 and

Interreg projects (co-funded by the European Regional Development Fund))

112

. On

average, EUR 1 billion of public funding (EU

113

and national) leveraged EUR 2.9 billion

of private investments in the course of the reporting period.

Significant cost reduction is still needed for tidal and wave energy technologies to exploit

their potential in the energy mix, for which intensified (i.e. increased rate of projects in

the water) and continued (i.e. continuity of projects) demonstration activities are

necessary. Despite advances in technology development and demonstration, the sector

faces a struggle in creating a viable market. National support appears low, reflected by

the limited commitment to ocean energy capacity in the NECPs compared to 2010 and

the lack of clear dedicated support for demonstration projects or for the development of

innovative remuneration schemes for emerging renewable technologies. This limits scope

for developing a business case and for identifying viable ways to develop and deploy the

technology. Specific business cases for ocean energy therefore need more focus, in

particular when its predictability can enhance its value, as well its potential for

decarbonising small communities and EU islands

114

. The upcoming offshore renewable

energy strategy offers an opportunity to support the development of ocean energy and

enable the EU to exploit its resources across the EU to the full.

3.3 Solar photovoltaics (PV)

Technology: solar PV has become the world’s fastest-growing energy technology, with

demand for solar PV spreading and expanding as it becomes the most competitive option

for electricity generation in a growing number of markets and applications. This growth

is supported by the decreasing cost of PV systems (EUR/W) and increasingly competing

cost of electricity generated (EUR/MWh).

The EU

115

cumulative PV installed capacity amounted to 134 GW in 2019, and it is

projected to grow to 370 GW in 2030, and to 1051 GW in 2050

116

. Given the significant

projected growth of PV capacity in the EU and globally, Europe should have a sizeable

role in the whole value chain. At the moment, European companies perform differently

across the various segments of the PV value chain (Figure 11).

Figure 11 European players across the PV industry value chain

112

JRC calculation, 2020.

113

EU funds awarded up to 2020 included UK recipients.

114

European Commission (2020), The EU Blue Economy Report, 2020.

115

EU including UK.

116

According to the projections in the Impact Assessment supporting the Climate Target Plan (COM(2020) 562 final.)

18

Source 11 ASSET study on competitiveness

Value chain: EU companies are competitive mainly in the downstream part of the value

chain. In particular, they have managed to remain competitive in the monitoring, control

and balance of system (BoS) segments, hosting some of the leaders in inverter

manufacturing and in solar trackers. EU companies have also maintained a leading

position in the deployment segment, where established players like Enerparc, Engie, Enel

Green Power or BayWa.re have been able to gain new market share worldwide

117

.

Furthermore, equipment manufacturing still has a strong base in Europe (e.g. Meyer

Burger, Centrotherm, Schmid).

Global market: the EU has lost its market share in some of the upstream parts of the

value chain (e.g. solar PV cell and module manufacturing). The highest value added is

located both a long way upstream (in basic and applied R&D, and design) and a long way

downstream (in marketing, distribution, and brand management). Even though the lowest

value-added activities occur in the middle of the value chain (manufacturing and

assembly), companies have an interest in being well positioned in these segments, to

reduce risks and financing costs. The EU still hosts one of the leading polysilicon

manufacturers (Wacker Polysilicon AG), whose production alone is sufficient to

manufacture 20 GW of solar cells, and which exports a significant part of its polysilicon

output to China

118

. Currently, global production of PV panels is valued at about EUR

57.8 billion, with the EU accounting for EUR 7.4 billion (12.8%) of that amount. The EU

still accounts for a relatively high share of the segment’s total value, thanks to the

production of polysilicon ingots. However, it has fallen back dramatically in the

manufacture of PV cells and modules. All the top 10 producers of PV cells and modules

now produce most of their output in Asia

119

.

117

ASSET Study on Competitiveness, 2020.

118

JRC PV Status Report, 2011.

119

Izumi K., PV Industry in 2019 from IEA PVPS Trends Report, ETIP PV conference “Readying for the TW era,

May 2019, Brussels

Market Size

(M€)

Equipment for

PV

manufacturing

Monitoring &

Controls

Solar PV

panels (Silicon,

Cells, Modules)

EPC

Balance of

system

Deployment

Key players

EU

• Valoe

• Centrotherm

• SCHMID

• Hanwha Q-cells

(Partially EU)

• Wacker Chemie

• 3Sun

• GreenPower

Monitoring

• AlsoEnergy

(partially EU)

• Solar-log

• Meteo&Control

Inverters

• SMA

Trackers

• Soltec

Highly fragmented

market dominated by

local players

• Enel Green Power

• Engie

• BayWa.re

Market

Growth

Outlook

R&D directed to HJT Focus on increasing

cell efficiency

Focus diagnostics

and optimisation

Increasing

warranties and cost

reduction

Focus on factory vs

field work

Access to low cost

capital and leading

technology is key

Critical

materials

None

Silver, Copper

None None None None

Key

activities

• PV manufacturing

equipment

• New PV technology

development

• Manufacturing of

silicon ingots, cells

and PV modules

• Developing

hardware and

software to improve

the performance of

solar farm

• All non-module

hardware (Inverters,

Trackers, Steel

structures, cabling,

etc.)

• Engineering design

• Construction

• Lease & Insurance

• Commissioning

• Development

• Finance

• O&M

57.842

7.368

EUGlobal

1.329

66

Global EU

2.694

678

Global EU

25.707

3.275

EUGlobal

17.995

2.292

EUGlobal

26.993

3.438

Global EU

EU: Global:

Key players

Rest of the

World

• Meyer Burger

• Trina Solar

• Jinko Solar

• GCL-Si

• Hanwha Q-cells

(Partially KR)

• JA Solar

• Longi

• Tongwei

• AlsoEnergy

(Partially US)

• Inaccess

Inverters

• Huawei

• SunGrow

Trackers

• Nextrack

er

• Array

Tech

Highly fragmented

market dominated by

local players

• Nexterra

• BP Lightsource

>15% >10% >5% >0%

Legend:

(10 year CAGR)

EU: Global: EU: Global: EU: Global: EU: Global: EU: Global:

19

Capital expenditure costs for polysilicon, solar cell and module manufacturing plants fell

dramatically between 2010 and 2018. Together with innovations in manufacturing, this

should offer an opportunity for the EU to take a fresh look at the PV manufacturing

industry and reverse the situation

120

.

The EU’s presence in the far upstream and far downstream parts of the value chain could

well provide a basis for rebuilding the PV industry. This would require a focus on

specialisation or high-performance/high-value products, such as equipment and inverter

manufacturing and PV products tailored to the specific needs of the building sector,

transport (vehicle integrated PV) and/or agriculture (dual land use with AgriPV), or to

the demand for high-efficiency/high-quality solar power installations to optimize use of

available surfaces and of resources. The modularity of the technology makes it easier to

integrate PV in a number of applications, especially in the urban environment. These

novel PV technologies, which are now reaching the commercial phase, could offer a new

basis for rebuilding the industry

121

. The strong knowledge of the EU research institutions,

the skilled labour force, and the existing and emerging industry players provide a basis

for re-establishing a strong European photovoltaic supply chain

122

. To remain

competitive, such industry needs to develop a global outreach. Building a sizeable EU

PV manufacturing industry would also reduce the risk of supply disruptions and quality

risks.

3.4 Renewable hydrogen production through electrolysis

This section focuses on renewable hydrogen production and on the competitiveness of

this first segment of the hydrogen value chain

123

. Hydrogen is key to to store energy

produced by renewable electricity and to decarbonise sectors that are hard to electrify.

The aim of the EU hydrogen strategy is to integrate 40 GW of renewable hydrogen

124

electrolysers and the production of up to 10 Mt of renewable hydrogen in the EU energy

system by 2030, with direct investment of between EUR 24 billion and EUR 42

billion

125

,

126

.

Technology: the capital cost of electrolysers has fallen by 60% in the last decade, and is

expected to halve again by 2030, compared to the present day, thanks to economies of

120

Arnulf Jäger-Waldau, Ioannis Kougias, Nigel Taylor, Christian Thiel, How photovoltaics can contribute to GHG

emission reductions of 55% in the EU by 2030, Renewable and Sustainable Energy Reviews,

Volume 126, 2020, 109836, ISSN 1364-0321

121

Here are a few examples of the most relevant PV manufacturing initiatives in Europe. i) The H2020 ‘Ampere’

project supporting the construction of a pilot line to produce heterojunction silicon solar cells and modules. The 3Sun

Factory (Catania, Italy) produces one of the most efficient PV technologies based on this approach. ii) The Oxford PV

initiative for manufacturing PV solar cells based on perovskite materials, receiving an EIB loan under the InnovFin

EDP facility. iii) Meyer Burger’s patent-protected heterojunction/SmartWire technology, which is more efficient than

the current standard mono-PERC, as well as other heterojunction technologies currently available.

122

Assessment of Photovoltaics (PV) Final Report, Trinomics (2017).

123

On-site hydrogen production for co-located consumption in industrial applications appears to be a promising pattern

which could enable the scale for the wider introduction of the carrier in the energy system to be reached fast, in

line with the ambition of a climate-neutral economy and the hydrogen strategy. The competitiveness of the other

supply chain segments, such as the transport of hydrogen, its storage and its conversion in end-use applications

(e.g. mobility, buildings) is not dealt with in this report. The Commission has set up the European Clean

Hydrogen Alliance as a stakeholder platform to bring the relevant players together.

124

Renewable hydrogen (often referred to as ‘green hydrogen’) is hydrogen produced by electrolysers powered by

renewable electricity, through a process in which water is dissociated into hydrogen and oxygen.

125

A hydrogen strategy for a climate-neutral Europe, https://ec.europa.eu/energy/sites/ener/files/hydrogen_strategy.pdf

126

In addition, from now to 2030, an amount between EUR 220bn and EUR 340bn would be required to scale up and

connect 80-120 GW of solar and wind generators to the electrolysers to supply the necessary electricity.

20

scale

127

. The cost of renewable hydrogen

128

currently lies between EUR 3 and EUR 5.5

per kilo, making it more expensive than non-renewable hydrogen (EUR 2 (2018) per kilo

of hydrogen

129

).

Today, less than 1% of world hydrogen production comes from renewable sources

130

.

Projections for 2030 locate the cost of renewable hydrogen in the range of EUR 1.1-

2.4/kg

131

, which is cheaper than low-carbon fossil-based hydrogen

132

, and nearly

competitive with fossil-based hydrogen

133

.

Between 2008 and 2018, the Fuel Cells and Hydrogen Joint Undertaking (FCH JU)

supported 246 projects across several hydrogen-related technological applications,

reaching a total investment figure of EUR 916 million, complemented by EUR 939

million of private and national/regional investments. Under the Horizon 2020 programme

(2014-2018), over EUR 90 million was allocated to developing electrolysers,

complemented by EUR 33.5 million of private funds

134

,

135

. At national level, Germany

has deployed most resources, with EUR 39 million

136

allocated to projects devoted to

electrolyser development between 2014 and 2018

137

. In Japan, Asahi Kasei received a

multimillion dollar grant supporting the development of their alkaline electrolyser

138

.

Asia (mostly China, Japan and South Korea) dominates the total number of patents filed

between 2000 and 2016 for the hydrogen, electrolyser and fuel cell groupings.

Nevertheless, the EU performs very well and has filed the largest number of ‘high-value’

patent families in the fields of hydrogen and electrolysers. Japan, however, has filed the

largest number of ‘high-value’ patent families in the field of fuel cells.

127

From the hydrogen strategy: based on cost assessments by the IEA, IRENA and BNEF. Electrolyser costs to decline

from EUR 900/kW to EUR 450/KW or less in the period after 2030, and EUR 180/kW after 2040. The costs of

carbon capture and storage increase the costs of natural gas reforming from EUR 810/kWH2 to EUR 1512/kWH2.

For 2050, the costs are estimated at EUR 1152/kWH2 (IEA, 2019).

128

State of art for alkaline electrolyser efficiency is around 50 kWh/kgH2 (about 67% based on hydrogen lower

heating value (LHV)) and 55 kWh/kgH2 (about 60% based on hydrogen LHV) for PEM electrolysis. Energy

consumption for SOE is lower (of the order of 40 kWh/kgH2), but a source of heat is required in order to provide

the necessary high temperatures (>600°C).

https://www.fch.europa.eu/sites/default/files/MAWP%20final%20version_endorsed%20GB%2015062018%20%

28ID%203712421%29.pdf

129

https://www.iea.org/data-and-statistics/charts/hydrogen-production-costs-using-natural-gas-in-selected-regions-

2018-2 Original figure 1.7 USD - Conversation rate used: (EUR 1 = USD 1.18)

130

International Energy Agency, Hydrogen Outlook, June 2019, p. 32 – 2018 estimates.

131

COM(2020) 301 final

132

Refers to fossil-based hydrogen with carbon capture’ which is a subpart of fossil-based hydrogen, but where

greenhouse gases emitted as part of the hydrogen production process are captured.

133

Refers to hydrogen produced through a variety of processes using fossil fuels as feedstock COM(2020) 301 final.

134

JRC 2020‚ Current status of Chemical Energy Storage Technologies’, p. 63.

https://publications.jrc.ec.europa.eu/repository/bitstream/JRC118776/current_status_of_chemical_energy_storage

_technologies.pdf

135

Compared with EUR 472 million for FCH JU funding overall and EUR 439 million for other sources of funding.

136

This includes both private and public funds.

137

JRC 2020 ‚Current status of Chemical Energy Storage Technologies’, p. 63

https://publications.jrc.ec.europa.eu/repository/bitstream/JRC118776/current_status_of_chemical_energy_storage

_technologies.pdf

138

Yoko-moto, K., Country Update: Japan, in 6th International Workshop on Hydrogen Infrastructure and

Transportation, 2018.

21

Value chain: the main water electrolysis technologies are alkaline electrolysis (AEL),

polymer electrolyte membrane electrolysis (PEMEL) and solid oxide electrolysis

(SOEL)

139

:

- AEL is a mature technology with operational costs driven by electricity costs and high

capital cost. The research challenges are high-pressure operation and the coupling

with dynamic loads.

- PEMEL can reach significantly higher current densities

140

than AEL and SOEL, with

the potential to further reduce capital cost. In recent years, several large (MW-scale)

plants have been installed in the EU (in Germany, France, Denmark, and the

Netherlands), enabling the EU to catch up on AEL. It is a market-ready technology

with research mainly focused on increasing aerial power density, while guaranteeing

the simultaneous reduction of critical raw material use

141

and durability performance.

- SOEL exhibits greatest efficiency. However, plants are relatively smaller, usually still

in the 100 kW capacity range, require steady operation, and need to be coupled to a

heat source

142

. Overall, SOEL is still in the development phase, although it is possible

to order products on the market.

In 2019, the EU had around 50 MW of water electrolysis capacity installed

143

(about 30%

AEL and 70% PEMEL), of which about 30 MW were located in Germany in 2018

144

.

AEL has no critical components in its supply chain. Thanks to technical similarities with

the chlor-alkali electrolysis industry, which deploys much larger installations, it can

exploit technology overlap and benefit from well-established value chains.

145

. PEMEL

and SOEL share some cost and supply risks with the respective fuel cell value chains

146

.

This applies in particular to critical raw materials

147

in the case of PEMEL, and to rare

earths in the case of SOEL.

PEMEL has to withstand corrosive environments and therefore requires the use of more

expensive materials, such as titanium for bipolar plates. The main system-cost

contributors are the electrolyser stack

148

(40-60%), followed by the power electronics

(15-21%). The core components driving up the stack cost are the layers of membrane

electrode assemblies (MEA), which contain noble metals

149

. Cell components based on

rare earths that are used for SOEL electrodes and electrolyte are the main contributors to

139

A novel type of high temperature electrolyser, at a very low TRL, is under development: proton ceramic

Eeectrolysers (PCEL), with the potential advantage of producing pure dry pressurised hydrogen at the maximum

pressure of the electrolyser, unlike other electrolyser technologies.

140

Electrolysis is a surface-based process. Therefore, upscaling an electrolyser stack cannot take advantage of a

favourable surface/volume ratio as for volume-based processes. All other things remaining equal, doubling or

tripling the size of an electrolysis stack will almost double or triple the investment cost, with limited direct

economies coming from the scale-up. This is why the increased areal power density allowed in the PEMEL

approach is relevant. Obtaining higher hydrogen production for a given surface area of the electrolyser reduces the

capital cost and the overall footprint of the installation.

141

Mainly platinum group metals (PGMs), iridium in particular.

142

A recently started European project

142

is currently aiming to install 2.5 MW in an industrial environment.

143

https://iea.blob.core.windows.net/assets/a02a0c80-77b2-462e-a9d5-1099e0e572ce/IEA-Hydrogen-Project-

Database.xlsx

144

https://www.dwv-info.de/wp-content/uploads/2015/06/DVGW-2955-Brosch%C3%BCre-Wasserstoff-RZ-

Screen.pdf

145

https://www.fch.europa.eu/sites/default/files/Evidence%20Report%20v4.pdf

146

https://publications.jrc.ec.europa.eu/repository/handle/JRC118394

147

Iridium is currently crucial for PEM electrolysis only, but not for fuel cell systems. Since it is one of the rarest

elements in the earth’s crust, it is likely that any strain brought about by an increased additional demand will have

strong repercussions on availability and price.

148

A stack is the sum of all the cells.

149

https://www.fch.europa.eu/sites/default/files/Evidence%20Report%20v4.pdf

22

stack cost. It is estimated that stacks account for about 35% of overall SOEL system

cost

150

.

Global market: European companies are well-placed to benefit from market growth. The

EU has producers of all three main electrolyser technologies

151

, and is the only region

offering a well-defined market product for SOEL. The other players are located in the

UK, Norway, Switzerland, the US, China, Canada, Russia and Japan.

The global turnover for water electrolyser systems is currently estimated to be in the

range of EUR 100 to EUR 150 million per year. According to 2018 estimates, water

electrolysis production could reach a capacity of 2 GW per year (globally), within a very

short space of time (one to two years). European manufacturers could potentially supply

about one third of this increased global capacity

152

.

The aim of the EU’s hydrogen strategy is to achieve a significant renewable hydrogen

production capacity by 2030. This will require a tremendous effort to scale up from the

50 MW of water electrolysis capacity currently installed to 40 GW by 2030, with the

setting up of the capacity required for a sustainable value chain in the EU. This effort

should build on the innovation potential offered by the whole spectrum of the electrolyser

technologies and on the leading position EU companies have in electrolysis in all