Eionet Report - ETC/CME 2019/8

Renewable energy in Europe — 2019

Recent growth and knock-on effects

Authors: Filippo Capizzi (Vito), Anjana Das (Vito), Tom Dauwe (Vito), Ils Moorkens (Vito), Risto Juhana

Saarikivi (CHMI) and Mihai Tomescu (EEA)

ETC/CME consortium partners: AETHER, Interprofessional Technical Centre for Studies on Air

Pollution (CITEPA), Czech Hydrometeorological Institute (CHMI), Energy and Environmental

Studies and Software Development (EMISIA), Institute for Applied Ecology (ÖKO-INSTITUT),

ÖKO-RECHERCHE, Norwegian Institute for Air Research (NILU), Netherlands Environmental

Assessment Agency (PBL), National Institute for Public Health and the Environment (RIVM),

Environment Agency Austria (UBA), Flemish Institute for Technological Research (VITO)

Eionet Report - ETC/CME 2019/8

Legal notice

The contents of this publication do not necessarily reflect the official opinions of the European Commission or other institutions

of the European Union. Neither the European Environment Agency, the European Topic Centre on Climate change mitigation and

energy nor any person or company acting on behalf of the Agency or the Topic Centre is responsible for the use that may be made

of the information contained in this report.

Copyright notice

© European Topic Centre on Climate Change Mitigation and Energy (2019)

Reproduction is authorized provided the source is acknowledged.

More information on the European Union is available on the Internet (http://europa.eu).

European Topic Centre on Climate

change mitigation and energy

Boeretang 200

B-2400 Mol, Belgium

Tel.: +32 14 33 59 77

Email: [email protected]

Eionet Report - ETC/CME 2019/8

Contents

1 Introduction.............................................................................................................................................. 6

1.1 Background: international and European context ........................................................................ 6

1.2 About this report ........................................................................................................................... 8

1.2.1 Geographical scope.............................................................................................................. 9

1.2.2 Data sources and methodologies ........................................................................................ 9

2 Developments in renewable energy sources in Europe ......................................................................... 12

2.1 Recent progress in deployment of renewable energy sources ................................................... 13

2.1.1 Renewable energy shares at the EU level and in individual Member States .................... 13

2.1.2 Renewable electricity capacities per capita and per unit of gross domestic product ....... 14

2.2 Contributions of renewable energy sources by energy market sector and technology ............. 16

2.2.1 Contribution of renewable energy sources to various energy market sectors in Member

States 16

2.2.2 Renewable electricity ........................................................................................................ 17

2.2.3 Renewable heating and cooling......................................................................................... 27

2.2.4 Renewable transport fuels ................................................................................................ 31

3 Impacts on fossil fuel consumption, greenhouse gas emissions and air pollutant emissions ............... 35

3.1 Avoided fossil fuel use ................................................................................................................. 36

3.1.1 Effects at the EU level ........................................................................................................ 36

3.1.2 Effects at the Member State level ..................................................................................... 38

3.2 Gross avoided greenhouse gas emissions ................................................................................... 38

3.2.1 Effects at the EU level ........................................................................................................ 38

3.2.2 Effects at Member State level ........................................................................................... 41

3.3 Statistical impacts of renewable energy sources on primary energy consumption ................... 43

3.3.1 Effects at EU level .............................................................................................................. 43

3.3.2 Effects at Member State level ........................................................................................... 44

3.4 Gross effect on air pollutant emissions ....................................................................................... 45

3.4.1 Effects at EU level .............................................................................................................. 45

3.4.2 Effects at Member State level ........................................................................................... 46

3.5 Indirect effects by renewable energy technology ....................................................................... 52

4 EU developments in renewable energy sources in a global perspective ............................................... 56

4.1 Renewable electricity capacities by region and main source ..................................................... 57

4.1.1 Renewable electricity development by region .................................................................. 57

4.1.2 Wind and solar photovoltaic capacity deployment ........................................................... 61

4.2 Renewable energy investments .................................................................................................. 64

4.2.1 Share in global renewable energy investments................................................................. 65

Eionet Report - ETC/CME 2019/8

4.2.2 Growth in renewable energy investments ........................................................................ 66

4.2.3 Total new investments by technology ............................................................................... 68

4.3 Renewable energy employment ................................................................................................. 69

5 Glossary and abbreviations .................................................................................................................... 71

6 References .............................................................................................................................................. 74

Annex 1 Effects of renewable energy on GHG emissions and energy consumption ............................ 78

Annex 2 Effects of renewable energy on air pollutant emissions ......................................................... 80

Annex 3 Methodology and data sources for calculating approximated RES shares ............................. 82

Annex 4 Discussion of main 2017/2018 changes by sector and country .............................................. 83

Eionet Report - ETC/CME 2019/8

Acknowledgements

This report was prepared by the European Environment Agency (EEA) and its European Topic Centre on

Climate change Mitigation and Energy (ETC/CME). The ETC/CME is a consortium of European institutes

assisting the EEA to support European Union (EU) policy in the field of air pollution and climate change

mitigation.

Mihai Tomescu (EEA) and Ils Moorkens (ETC/CME) ensured the coordination of this report.

The authors were, in alphabetical order, Filippo Capizzi (Vito), Anjana Das (Vito), Tom Dauwe (Vito), Ils

Moorkens (Vito), Risto Juhana Saarikivi (CHMI) and Mihai Tomescu (EEA).

The project coordinators would like to thank Adrian Whiteman, from the International Renewable Energy

Agency (IRENA), for his cooperation and for the global data sets concerning renewable energy. We also

wish to thank Eurostat for allowing us to use the SHARES questionnaire templates to calculate and compile

the early renewable energy sources estimates (2018 RES proxies) and especially Marek Sturc (Eurostat) for

the support received for converting the methodology to the format of the new energy balances. We are

also grateful to Dr Wolfgang Schöpp and to Dr Janusz Cofala (IIASA) for the provision of the detailed GAINS

data and for their help in understanding the data.

The EEA would like to thank the national focal points and experts of the EEA member countries for their

cooperation and support during the preparation of this report. The EEA also acknowledges the comments

and suggestions received from experts from the European Commission and its Joint Research Centre and

wishes to thank them for their collaboration.

Eionet Report - ETC/CME 2019/8 1

Executive summary

This report outlines the progress made in 2017 in the deployment of renewable energy sources (RES) in

the European Union (EU) as a whole, and at country, market and technology level.

The results confirm that the EU RES share has remained in line with the indicative trajectory designed to

achieve the mandatory EU RES targets for 2020: a 20 % RES share in energy consumption and the sub-

target of 10 % RES for transport. However, to achieve these objectives with certainty, further efforts to

deploy renewable energy sources across the EU are needed, in particular given the rebound in final energy

consumption in some EU Member States in recent years.

The additional consumption of renewable energy sources throughout Europe since 2005, has had a

number of side benefits: it enabled the EU to reduce its demand for fossil fuels

1

with more than 12 % and

the associated greenhouse gas emissions (GHG) with 10 %, than if renewable energy sources had remained

at the same level as in 2005. For the effect on air pollutant emissions, the outcomes are mixed: the

additional consumption of RES since 2005 led to decreases in the emissions of NO

x

and SO

2

, but to

increases in the emissions of PM

10

, PM

2,5

and VOCs, mainly due to the combustion of biomass.

Besides calculations based on RES consumption data reported by Member States, the report also provides

early estimates from the European Environment Agency (EEA) for all these developments in 2018.

In the final part, the global perspective is taken into account. It indicates that the EU transformed its energy

production base between 2005 and 2017 at a speed which surpassed that of other world regions. Although

the EU is still the world leader in sustainable energy capacity per capita, it was surpassed by China in terms

of total installed capacity since 2013.

The renewable energy share has been continuously increasing at EU level

RES are a major contributor to the transition of Europe’s energy sector. The rapid development of some

renewable energy technologies has already allowed these technologies to achieve high market shares.

Today, for solar photovoltaic (PV) electricity, biogas electricity and solid biomass used for heating and

cooling, these shares are above, or close to, the 2020 levels anticipated by countries in their national

renewable energy action plans (NREAPs), drafted in 2010. This has led to GHG emission reductions in the

EU electricity sector, in the consumption of energy for heating and cooling, and, to a lesser extent, in

transport.

Recent increases in final energy consumption in some Member States are slowing down the pace of

growth of the RES share across the EU

The EU-wide share of renewable energy in gross final EU energy use increased from 17.5 % in 2017 to an

expected 18.0 % in 2018, according to the EEA’s early estimates. Accordingly, the EU has met its indicative

trajectory for 2017-2018 as set out in the Renewable Energy Directive (RED). However, the average yearly

growth in the RES share slowed down in recent years, compared with the average annual pace of growth

recorded between 2005 and 2015. As shown elsewhere (EEA 2019), the slower RES progress in recent

years can largely be attributed to increasing energy consumption across Europe. Although installed

renewable capacity has continued to grow, the pace of growth has slowed down as more energy from

non-renewable sources is consumed. For the period 2015-2017, increases in final energy consumption

from all sources have led to a reversal in progress towards national and EU energy efficiency objectives for

2020. In 2018, preliminary estimates of the EEA show that final energy consumption increased again by

0.1 % compared with 2017, marking the fourth consecutive year of final energy consumption increases.

1

Primary fossil fuel consumption

Eionet Report - ETC/CME 2019/8 2

Today, the RES shares continue to vary widely between countries, ranging from over 30 % of gross final

energy consumption in countries such as Austria, Denmark, Finland, Latvia and Sweden to 10 % or less, in

Belgium, Cyprus, Luxembourg, Malta, and the Netherlands.

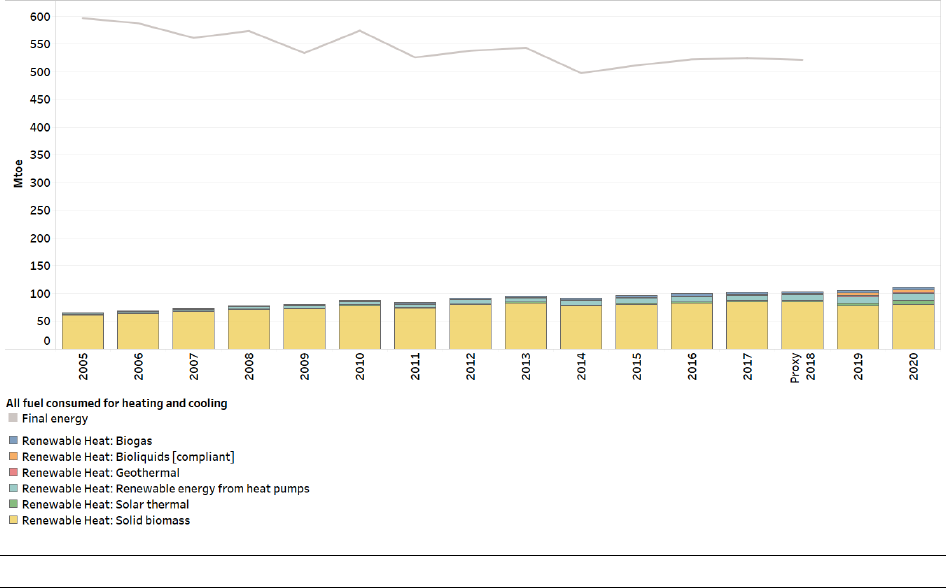

Renewable energy sources are mostly used for heating and cooling; in transport they are lagging behind

In absolute terms, renewable energy for heating and cooling remains the dominant RES market sector in

Europe. RES made up close to one fifth of all final energy consumed for heating and cooling: 19.5 % in 2017

and 19.8 % in 2018, according to reported data and early EEA estimates. Since 2005, despite biogas and

heat pumps having faster percentage points increases on average per year, solid biomass-based

technologies prevailed in this market sector.

In absolute terms, renewable electricity is the second largest RES market sector in the EU. Growth in this

sector was driven especially by growth in onshore and offshore wind power and solar PV electricity

generation, but also by other RES, such as an increase in solid biomass combustion for electricity purposes.

More than 30 % of all electricity consumed in the EU in 2017 and in 2018 (30.7 % and 32.1 % respectively)

originated from renewable sources.

The average renewable electricity capacity per capita for the EU more than doubled in 2017 compared

with 2005 (0.8 kWe per person in 2017), with large differences between Member States. A similar

development was observed for the average RES-E capacity per unit of gross domestic product (GDP). It

also more than doubled in 2017, compared with 2005 (29 kWe per million euro of GDP), but large

differences remain visible between the Member States.

In the EU transport sector, renewable energy made up 7.6 % of all energy use in 2017 and 8.1 % in 2018,

according to reported data and the EEA’s early estimates. With renewable electricity currently playing only

a small role in transport, the bulk of renewable energy use in this sector comes from biofuels. To prevent

potential negative impacts on climate, the environment and interactions with food production from land-

use (such as when natural forests and food crops are displaced by biofuels), only certified biofuels that

comply with the sustainability criteria under the RED can be counted towards the RED targets. Certification

is carried out through voluntary schemes recognised by the European Commission and through national

systems set up by the Member States.

Transport biofuels grew fastest over the period 2005-2017 (at 7 percentage points increase per year, on

average), as they increased from a very low level in 2005. Nevertheless, considerable efforts are needed

in this market sector in the run-up to 2020 to reach the 10 % RES target in transport by 2020 at the national

and at the EU level. A higher share of renewable electricity use in the transport sector would reduce the

pressure on transport biofuels to reach the EU’s target of a 10 % RES share consumed in transport by 2020.

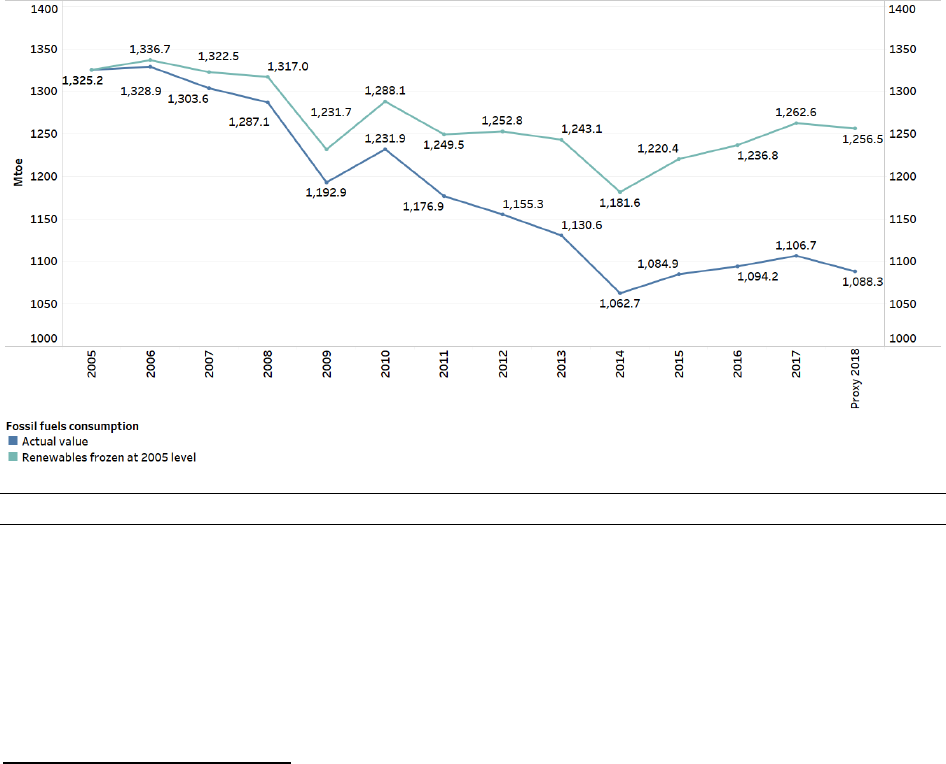

The increased use of renewable energy sources since 2005 allowed the EU to cut its fossil fuel use and

the associated greenhouse gas emissions by, respectively, 168 Mtoe and 543 Mt CO2 in 2018

The additional consumption of renewable energy compared with 2005 levels, allowed the EU to cut its

demand for fossil fuels by 156 million tonnes of oil equivalent (Mtoe) in 2017. This is equivalent to 11 % of

the EU’s gross inland consumption of fossil fuels and this amount is higher than the fossil fuel consumption

of the United Kingdom (see Figure 1). In 2018, the amount of substituted fossil fuels is estimated to have

increased by 12 Mtoe to a total of 168 Mtoe.

These fossil fuel savings due to the additional use of renewable energy after 2005 helped the EU achieve

an estimated gross reduction in CO

2

emissions of 502 Mt CO

2

(10 %) in 2017, compared with a

counterfactual scenario in which RES consumption would have stayed at the 2005 level. This almost

represents the annual GHG emissions of the United Kingdom. In 2018, the effect on CO

2

emissions

increased further, resulting in a gross emission reduction of 543 Mt CO

2

(an 11 % gross reduction in the

EU). Most of these changes took place in energy-intensive industrial sectors under the EU Emissions

Trading System (ETS), as the increase in renewable electricity decreased the reliance on fossil fuels and

made up roughly three quarters of the estimated total EU reductions.

Eionet Report - ETC/CME 2019/8 3

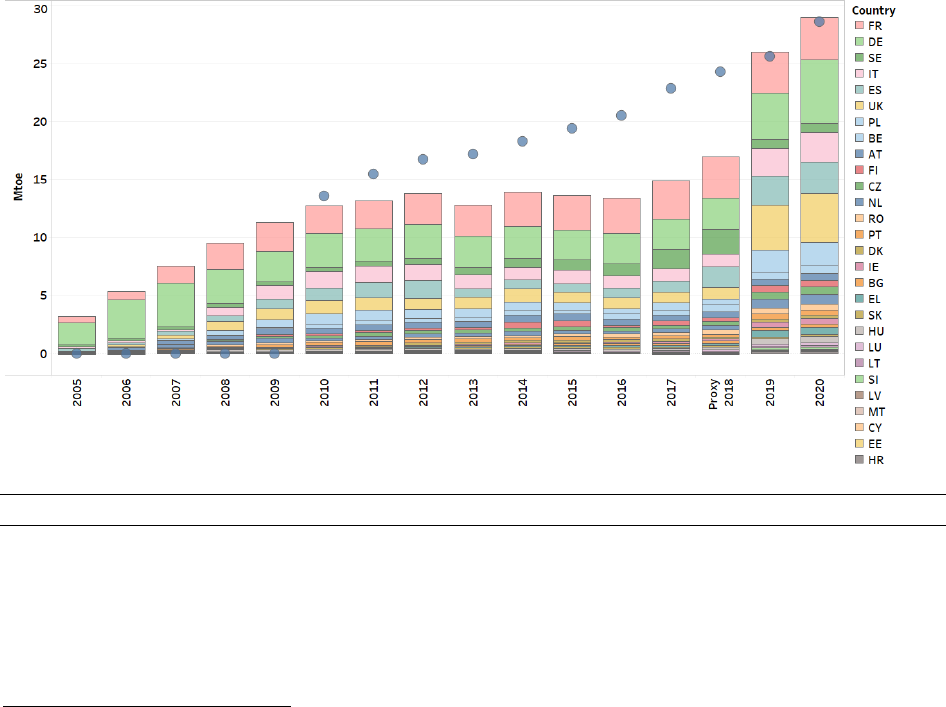

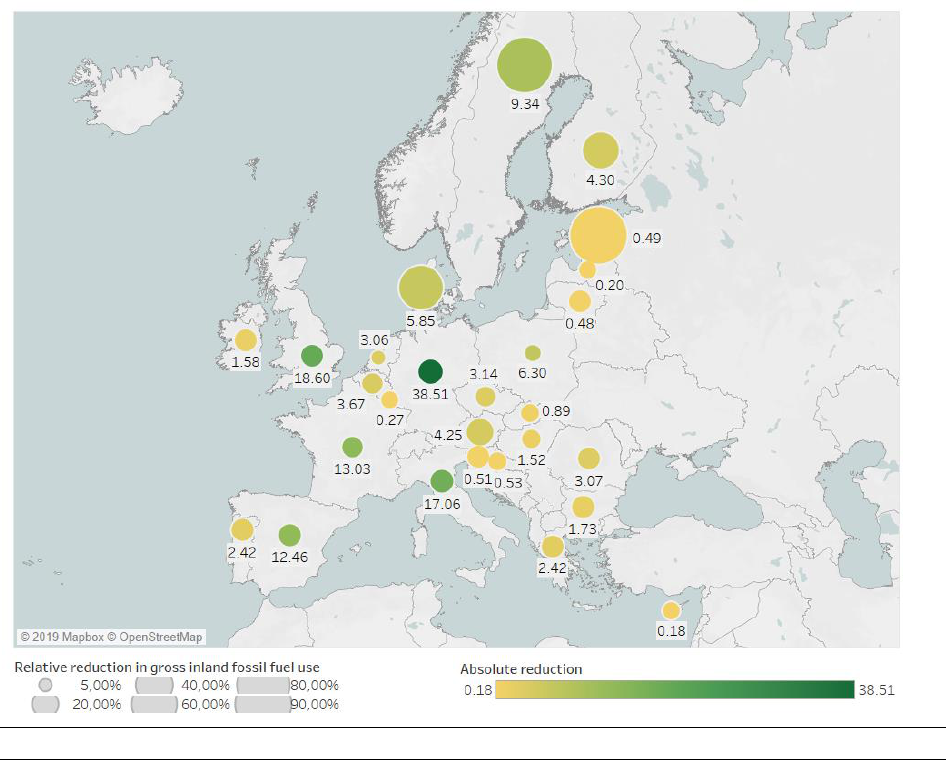

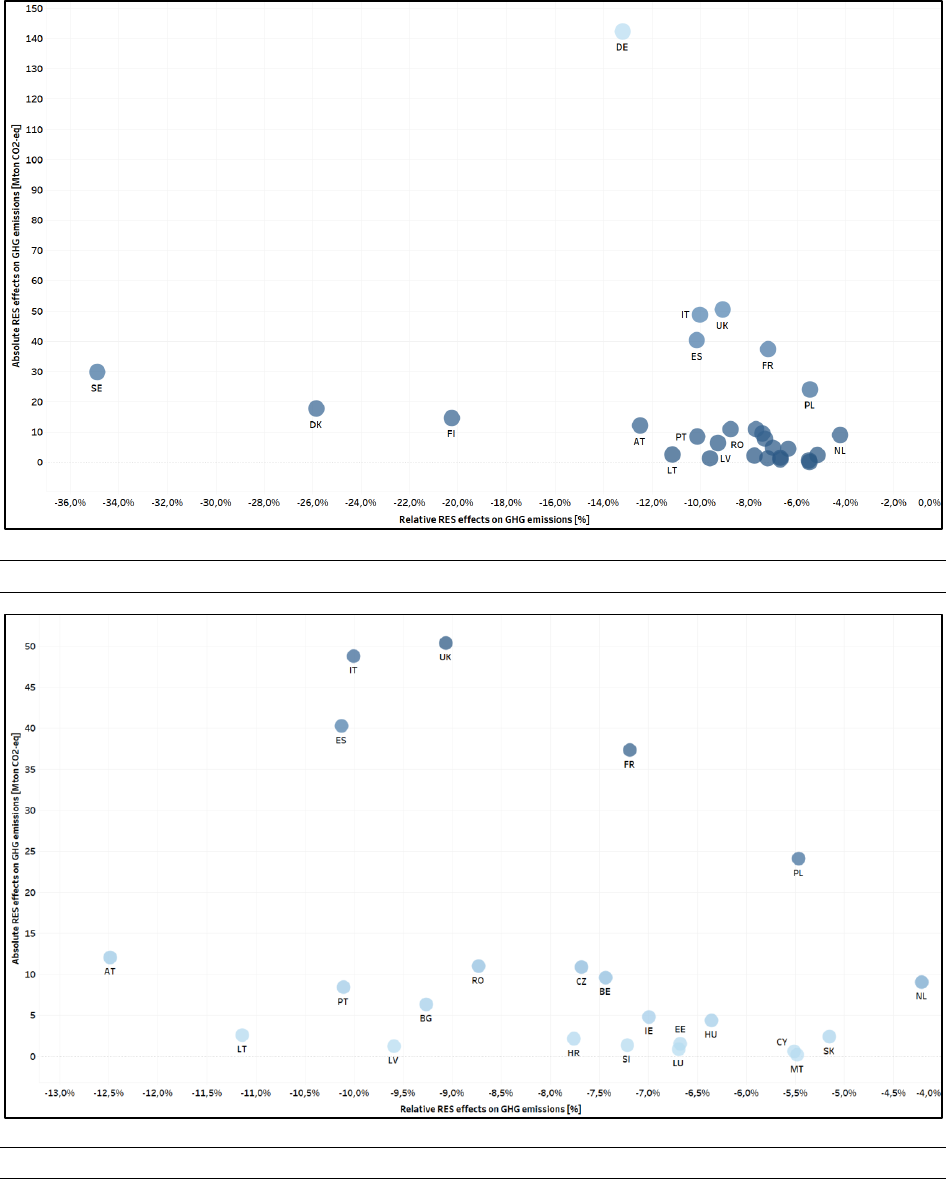

National RES deployment since 2005 led to the largest absolute reduction in domestic fossil fuel use and

avoided GHG emissions in Germany, Italy and the United Kingdom in both 2017 and 2018. However, in

terms of their overall effectiveness in substituting fossil fuels and reducing GHG emissions by increasing

their RES deployment three of the Nordic countries (Denmark, Finland and Sweden) remained the most

effective Member States in the EU in 2017 (see Figure 1).

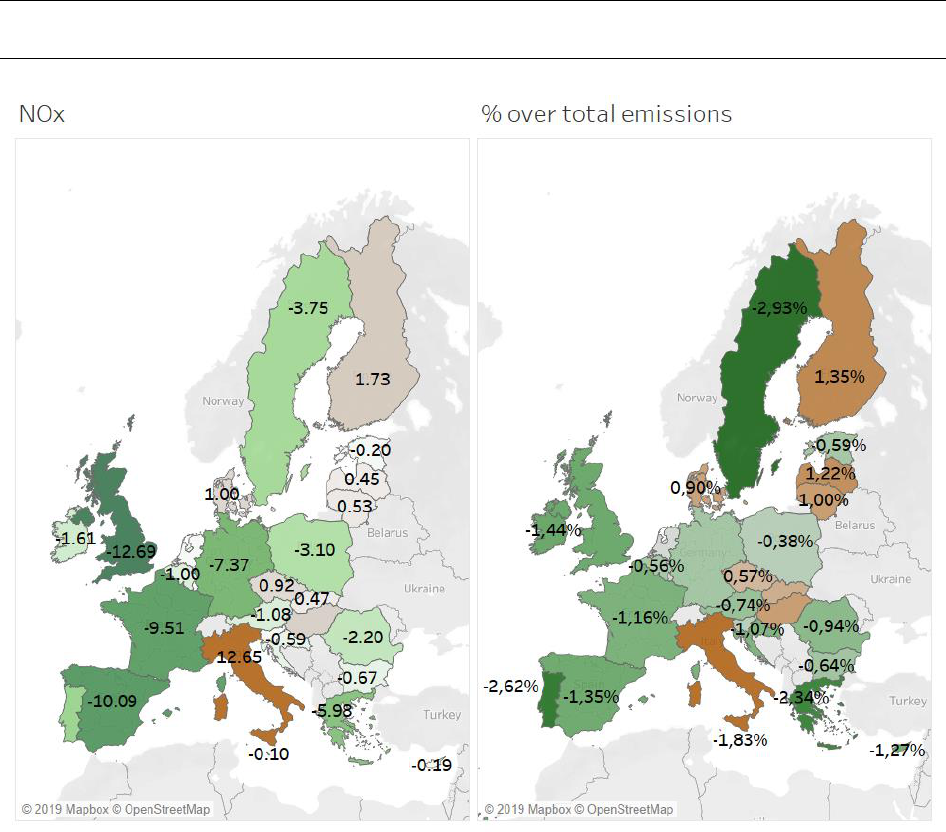

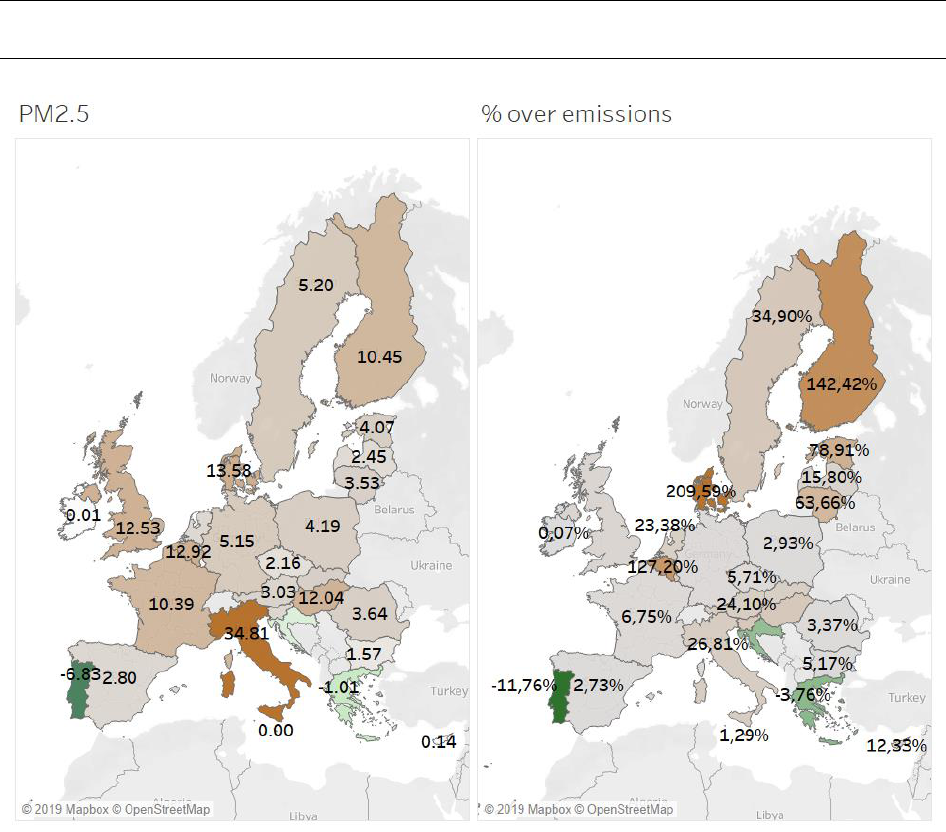

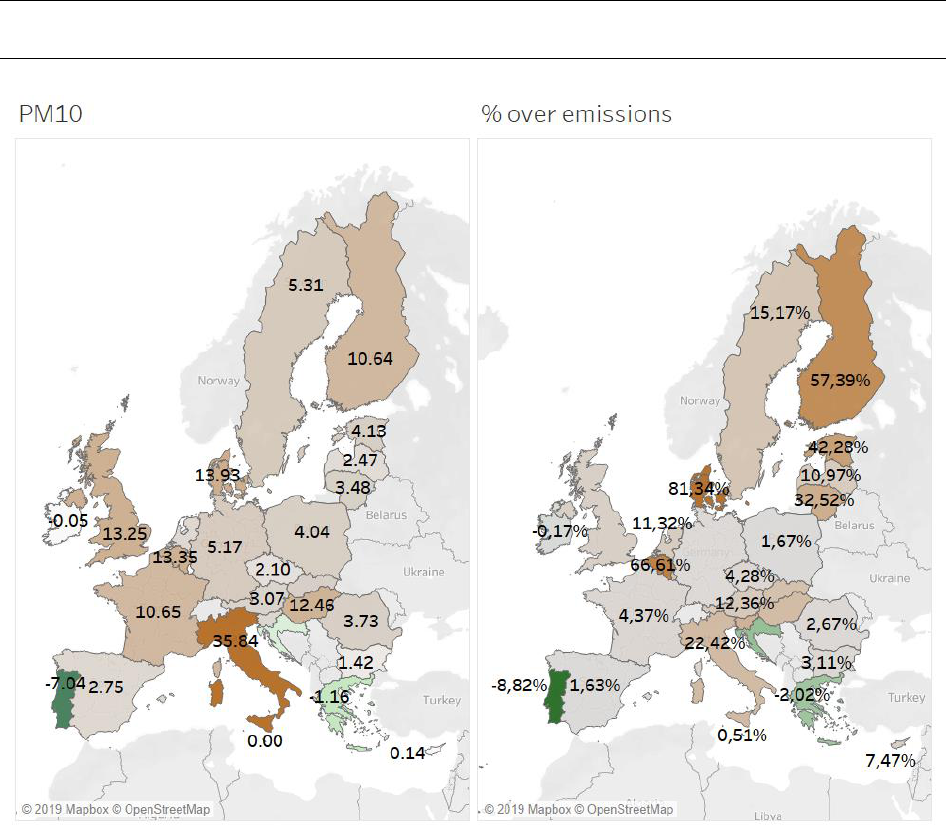

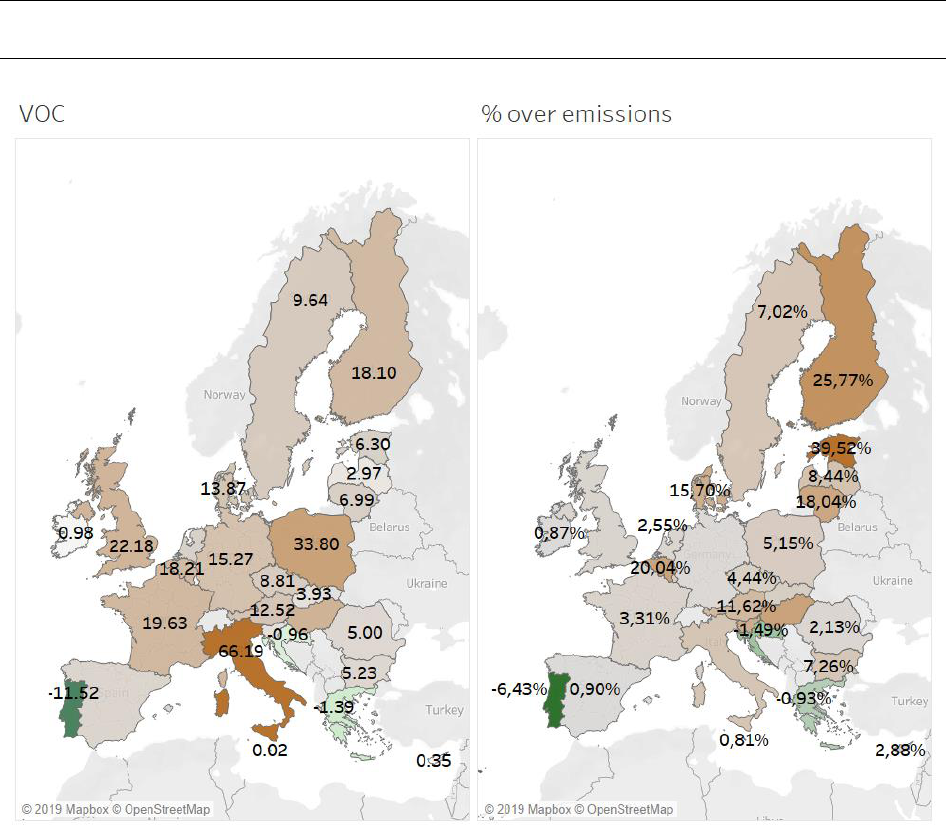

The increased use of renewable energy sources since 2005 allowed the EU to cut its emissions of NOx

and SO

2

, but caused an increase of PM and VOC emissions

At the EU level, for 2017, the total estimated RES effect results in a decrease of air pollutant emissions of

46 kt for NO

x

and 159 kt for SO

2

, compared with a counterfactual scenario in which RES consumption would

have remained at the levels of 2005. However, for PM

10

, PM

2.5

and VOCs emissions, the result is an increase

of respectively 149, 145 and 296 kt in 2017 compared with 2005. On the relative level, comparing to total

emissions frozen at 2005 level, the additional consumption of renewable energy sources across the EU

since 2005 has led to a decrease of SO

2

and NO

x

emissions in 2017, by 6 % and 1 %, respectively. In contrast,

an indicative increase of EU-wide emissions for PM and VOCs took place in 2017, following the increase in

biomass use since 2005 (by 13 % for PM

2.5

, 8 % for PM

10

and 4 % for VOCs).

Renewable energy has grown to account for more than 33% of the world’s total installed power

generating capacity in 2018

Renewable energy in power generation continued its strong pace in 2018. An estimated 171 GW was

installed worldwide, almost the same as 2017 additions, and total installed capacity grew more than 8%.

Renewables delivered more than one quarter (26 %) of the total global electricity generation in 2018.

Global investments in renewables have shown steady growth for more than a decade. This has led to a

more than doubling of global renewable electricity capacity between 2005 and 2018. By 2018, for the

fourth year in a row, more than half of all newly installed power capacity worldwide was of renewable

origin, as RES accounted for an estimated 70 % of added net power generation capacity in that year

(Frankfurt School-UNEP 2019; IRENA 2019a). In 2018, the EU still ranked second after China as regards

total installed and grid-connected domestic renewable electricity capacity.

Viewed from the perspectives of technology and the market sector, global RES development in 2018 was

dominated by high investment in solar and wind energy for electricity generation. Together, these

technologies accounted for over 80 % of total global RES investments (Frankfurt School-UNEP 2019). At

the other end, investments in biofuels (used mainly in transport) were lower in 2018 than in 2005, possibly

because interest in first-generation biofuel capacity is plateauing and second-generation biofuel

technologies still struggle to overcome technical and financial obstacles.

The EU is a global leader in renewable electricity capacity per capita, but fast activity becomes visible

outside the EU

With an average renewable electricity capacity of 0.82 kW installed per person in 2018, the EU is the clear

world leader on a per capita basis, ahead of the United States, Brazil and China. However, since 2017,

China has displaced the EU as market leader in solar PV capacity and in 2018, with 185 GW of installed

wind capacity, China displaced the EU also with regard to installed wind power capacity.

Over the period 2005-2018, the renewable electricity capacity installed per unit GDP in the EU grew faster

than the rate of growth in other world regions. In general, growth in renewable electricity capacity in the

EU has been particularly notable since 2009, which coincides with the adoption in 2009 of the EU climate

and energy package. However, countries such as China and India had higher growth rates in 2016-2017

than the EU. The recent agreement on the revised RED (EU 2018a), which sets the overall EU target for

RES to 32 % in 2030, and requires Member States to ensure via obligations on fuel suppliers that

renewables will reach a level of at least 14 % in transport by the same year, is expected to boost renewable

energy investments again in the EU.

Between 2005 and 2012, Europe recorded the highest annual shares of global new investments in

renewable power capacity. Despite declining from 46 % in 2005 to 15 % in 2017, these high annual shares

highlight Europe’s pioneering role in developing renewable energy globally. Since 2013, however, China

Eionet Report - ETC/CME 2019/8 4

has claimed the highest annual shares of global new investments in renewable power capacity. Moreover,

China registered a steep jump in its share in global investment, from 35 % in 2016 to 45 % in 2017.

However, the share declined to 32% in 2018, although China still dominates globally: global investment

activity is spreading to new attractive markets outside the EU.

Other countries are seeing faster progress in terms of the share of RES-related jobs per capita in the

labour force

The EU is also a key global player in terms of employment in the renewable energy sector, with an

estimated 1.2 million jobs related to renewables in 2018, or roughly 0.5 % of the total labour force (IRENA

2019b). In terms of proportion of renewable energy-related jobs in the labour force in 2018, it came fourth,

after Brazil, China and the United States. Within the EU, Germany was the number one employer in terms

of RES-related jobs per capita in the labour force, second only to Brazil on the global level.

The largest employers in the EU renewables sector are the wind, solar PV and solid biomass industries.

Following job losses since 2012, the total estimated employment of direct and indirect jobs in renewable

energy remained virtually the same in 2017 compared to 2016. However, this stable figure covers

fluctuations among technologies and countries. In 2017, employment grew in liquid biofuels, compared to

2016, but declined in all other renewables industries.

For 2030, Member States and the EU need to intensify their climate and energy efforts

To reach the EU climate and energy targets for 2030 and to become a sustainable, low-carbon economy

by 2050, Member States need to overcome a number of important challenges. In the short term, these

concern formulating adequate national decarbonisation targets and policy responses for 2030 that will

collectively deliver the EU’s climate and energy targets and the commitments under the international Paris

Agreement. In the medium term, Member States need to improve their national innovation capabilities to

increase benefits from the ongoing energy transition in Europe.

To maintain this momentum, the EU and its Member States should reinforce and build existing, home-

grown expertise and innovation capacity in renewable energy and energy efficiency solutions. This will

also help retain Europe’s global competitiveness in these growing knowledge-intensive sectors. To that

end, in 2018, the EU institutions agreed on a more systematic cooperation and coordination of national

policies and measures between Member States by adopting the RED II. The European Commission also

recently put forward a climate vision for 2050 (EC 2019b), which confirms the EU’s willingness to lead

global climate mitigation efforts and support the objective of full carbon neutrality by 2050.

Eionet Report - ETC/CME 2019/8 5

Figure 1 Total and relative reduction in gross inland fossil fuel use (per year, in 2017)

Notes: The absolute reduction in gross inland fossil fuel use in 2017, expressed in million tonnes of oil equivalent (Mtoe), is

proportional with the increase of renewable energy consumption achieved between 2005 and 2017. It represents the annual

estimate for 2017; the cumulative value over the period 2005 – 2017 is much larger. The relative reduction in gross inland fossil

fuel use is expressed as the absolute reduction over a country’s total gross inland consumption of fossil fuels.

Source: ETC/CME

Eionet Report - ETC/CME 2019/8 6

1 Introduction

1.1 Background: international and European context

Limiting global warming in line with the Paris Agreement (

2

) (UNFCCC 2015) to significantly reduce the risks

and the impacts of climate change requires fundamentally transforming our energy system and adjusting

our production and consumption patterns in just a few years.

Increased deployment of renewable energy sources (RES) plays an important role in mitigating climate

change and unfolding this transformation. With long-term energy demand overall stable or decreasing in

Europe, increasing the share of renewable sources of energy triggers the displacement of non-renewable

sources (especially fossil fuels) in power supply, heat production and transport, thereby reducing

greenhouse gas (GHG) emissions across all sectors. Renewables are thus a key pillar in delivering the

European Energy Union’s decarbonisation priority (see Box 1.1), achieving the EU’s climate commitments

under the Paris Agreement, and supporting the transition towards a greener, resource-efficient and more

competitive low-carbon EU economy and society by 2050.

To date, a broad set of complementary climate and energy policies support low-carbon energy

developments and aim to spur innovation in this field. Progress achieved in EU-wide renewable energy

deployment since 2005 is largely attributed to the presence of binding national targets for 2020 under the

Renewable Energy Directive, or RED (EU 2009), and to national support instruments put in place in

response to these targets, such as feed-in tariffs, feed-in premiums, auction/tender systems, quotas, tax

credits and grants.

Technological advances, the scaling up of global production volumes and a reduction in capital costs have

also each played an important role in lowering the costs of renewable energy, especially of wind power

and solar photovoltaic (PV) technologies (EC 2015; IRENA 2016). Nevertheless, the rapid initial

developments also triggered frequent adaptation of Member States’ policies to establish cost-effective

support and, in some cases, even to abrogate that support. As many of these changes fuelled uncertainty

on the markets, auction-based programmes have come to replace the initial subsidy-based support

measures in Europe, and increasingly globally, pushing renewable energy projects to become more cost-

competitive and contributing to further reductions in the costs of renewable energy projects (Frankfurt

School-UNEP 2019).

In recent years, however, the annual pace of growth in the EU has stagnated or decreased for most

renewable electricity (RES-E) technologies and for renewable heating (RES-H) from solar thermal and heat

pumps. It has continued to increase for only a few other renewable energy technologies (i.e. geothermal

and solid biomass-based technologies). This loss of speed initially took shape in the aftermath of the

financial crisis, when many support mechanisms were scaled back, sometimes cut entirely or were

retroactively changed. Subsequently, economic growth resumed across countries and, since 2015, energy

consumption from non-renewable sources increased by more than that from renewable ones, as a result

of increased energy use in the transport sector and low carbon prices in the EU’s electricity market. The

increasing number of countries getting closer to, or having reached their renewable energy targets for

2020 ahead of time, may offer a further explanation, in the context in which the recast of the RED (RED II)

(EU 2018a) sets a binding EU-level target for renewable energy consumption by 2030 (of 32 %) and invites

Member States to define their own national contributions to achieving that target as part of their

integrated national energy and climate plans (NECP) under the Energy Union Governance Regulation (EU

(

2

) The Paris Agreement’s central aim is to strengthen the global response to the threat of climate change by keeping

the global temperature rise this century well below 2 °C above pre-industrial levels and to pursue efforts to limit

the temperature increase even further to 1.5 °C. The Paris Agreement requires all Parties to put forward their

best efforts through ‘nationally determined contributions’ (NDCs) and to strengthen these efforts in the years

ahead (UNFCCC 2015).

Eionet Report - ETC/CME 2019/8 7

2018b). By the end of 2018, most Member States had submitted draft plans to the EC. Following that, in

June 2019 the EC issued recommendations on the draft plans; Member States have to consider these when

submitting their final NECPs, by the end of 2019.

The EC’s assessment of the draft plans shows that almost all Member States have submitted their

contributions to the EU renewable energy target. Almost a third of the Member States submitted

ambitious contributions. Despite that, there is still a gap in ambition when considering the EU’s target for

2030: under the current draft plans, the EU-wide share of renewable energy sources would reach between

30.4% and 31.9% in 2030, instead of at least 32% (EC 2019a). In addition to the lack of ambition in some

of the NECPs, another issue is the scarcity of indications in the plans on how to achieve the investments

for the needed renewable energy capacity.

However, to reach with certainty the mandatory 20 % share of EU renewable energy consumption by 2020

and the 10 % RES sub-target for the transport sector, in the context of the recent upwards trend in energy

consumption, sustained efforts and corresponding adaptation of national policies to promote renewable

energy projects will be indispensable in the very short run (EEA 2018b).

Box 1.1 EU renewable energy policies up to 2020 and 2030

The EU was an early adopter of renewable energy starting with the implementation of EU-wide policies from the

mid-nineties. After the first directive on electricity production from renewable energy sources (2001) with

indicative targets, the review (in 2005) of Member States’ supporting schemes led to a period of debate and

negotiations between Member States and the EU institutions. This resulted, in 2009, in the RED (2009/28/EC),

which set legally binding national targets contributing to an EU-wide target of 20 % renewable energy in the total

energy needs by 2020.

The binding national targets are set at different levels to reflect national circumstances. The EU’s renewable

energy target for transport (i.e. a 10 % share by 2020) is divided equally for all countries into 10 % national

targets, with biofuels produced from energy crops grown on agricultural land limited to a maximum of 7 %. The

RED also sets out options for cooperation to help countries achieve their targets cost-effectively.

In the run-up to 2020, two interim trajectories are of particular interest in assessing the EU’s and Member States’

progress towards their binding targets:

• The minimum indicative RED trajectories for each country. These trajectories concern only the total

RES share. They run until 2018, ending in 2020 with the binding national RES share targets. They are

provided in the RED to ensure that the national RES targets will be met.

• The expected trajectories, adopted by Member States in their national renewable energy action plans

(NREAPs) under the RED. These NREAP trajectories concern not only the overall RES share but also the

shares of renewables in the electricity, heating and cooling, and transport sectors up to 2020.

For 2030, the RED II sets a binding EU-wide target of 32 % RES in gross final energy consumption. Member States

have proposed an indicative level of effort contributing to the EU binding target for renewables in their draft

NECPs. The binding national RES targets for 2020 remain in the recast directive as baseline levels. The RED II also

includes:

• guiding principles concerning financial support schemes for RES-E;

• the requirement for Member States to set up ‘one-stop shops’ to coordinate the entire permit-granting

process for new RES generation, transmission and distribution capacity;

• principles of renewable self-consumption and (local) renewable energy communities;

• enhancement of existing provisions on cross-border cooperation;

• provisions to improve the sustainability and GHG emissions-saving criteria for biofuels, bioliquids and

biomass;

• mainstreaming of renewable heating and cooling (RES-H&C) applications, in particular by asking

Member States to increase the share of renewable energy supplied for heating and cooling by a fixed

rate (by an indicative 1.3 percentage points for 2021-2025 and higher thereafter) per year, starting from

the level achieved in 2020.

Eionet Report - ETC/CME 2019/8 8

Outlook beyond 2020

In June 2018, European countries gave their endorsement to a binding EU-wide renewable energy target

of a minimum of 32 % of gross final consumption by 2030, which is included in the recast Renewable

Energy Directive (RED II) that entered into force at the end of 2018. Building on the Energy Union strategy

of 2015 (EC 2015), as well as on the Regulation on the Governance of the Energy Union (EU 2018b) (

3

),

Member States had to propose an indicative level of effort contributing to the EU binding target for

renewable energy as part of their draft integrated national energy and climate plans, by the end of 2018.

Following the Commission’s recommendations of June 2019, as necessary, Member States have to

heighten their contributions in their final plans due at the end of 2019.

The increased target for renewable energy (original target of at least 27 %, revised upwards to 32 % in

2018) as well as the increased target for energy efficiency (original target 27 %, revised upwards to 32.5 %

in 2018) by 2030 are important in light of the “at least 40%” greenhouse gas emission reduction. Together

these targets form the backbone of the 2030 climate and energy framework which was adopted by the

European Council in October 2014.

Since the renewable energy target is defined as the share of renewable energy in gross final energy

consumption it is clear that the role of energy savings and improved energy efficiency in gross final

consumption cannot be underestimated.

In the run-up to 2030, the indicative RES trajectory of the EU (based on the collective efforts of the Member

States) should reach at least the following reference points for the total increase in the RES share between

the binding 20 % RES share target for 2020 and the binding 32 % RES share target for 2030: 18 % by 2022;

43 % by 2025; 65 % by 2027. Should Member States fall behind similar reference points in relation to their

RES trajectories in the integrated national energy and climate plans, they will need to implement additional

measures to cover the gap within 1 year (EU 2018b). The RED II intends to mainstream renewable energy

in heating and cooling and thus includes a trajectory for this purpose. Member States are urged to make

an effort to increase the share of renewable energy by an indicative 1.3 percentage points as an annual

average calculated for the periods 2021 to 2025 and 2026 to 2030, starting from the share of renewable

energy in the heating and cooling sector in 2020, expressed in terms of national share of final energy

consumption. The increase shall be limited to an indicative 1.1 percentage points for Member States where

waste heat and cold is not used (EU 2018a).

Beyond Europe

In the past, the EU has been a frontrunner in renewable energy. Nevertheless, with developing countries

investing more in green energy than developed economies, the situation may be changing in the short run

(see Chapter 1).

1.2 About this report

This EEA report depicts changes in RES in Europe since 2005, at the level of individual technologies and

countries (Chapter 2) and outlines key global developments to put European progress in perspective

(Chapter 1). It also illustrates the co-benefits of growing RES consumption in Europe, notably the

replacement of fossil fuels by a growing share of renewables and the resulting effects on the reduction in

GHG emissions and air pollutant emissions (Chapter 0). This chapter sets the overall context.

The assessment uses Eurostat data for the period 2005-2017, complemented by early EEA estimates

regarding GHG emissions and energy developments in 2018.

(

3

) The Regulation on the Governance of the Energy Union, which entered into force at the end of 2018, is a

horizontal piece of legislation that aims to streamline monitoring and reporting of progress, and increase

synergies and cooperation across all dimensions of the Energy Union, so as to obtain a high level of policy

coherence through integrated national energy and climate plans.

Eionet Report - ETC/CME 2019/8 9

1.2.1 Geographical scope

Owing to the limited availability of primary data, this assessment focuses on the 28 EU Member States

(EU-28). In Chapter 1, capacities and investments in RES-E are aggregated into relevant world regions to

facilitate a comparison of the EU’s progress with international developments. Details of the geographic

aggregation are presented in the glossary.

1.2.2 Data sources and methodologies

Approximated estimates for the share of gross final consumption of renewable energy resources (RES

share proxies)

The EEA 2018 RES shares are, ultimately, estimated values. Although the 2018 RES shares proxies formed

the basis of a specific EEA country consultation, carried out in September 2019 (

4

), these values are not a

substitute for data that countries officially report to Eurostat.

The methodology applied for approximating RES values in the year t-1 was described in a previous EEA

report (EEA 2015) — see also Annex 3. Confidence in the estimated RES share proxy values is greatest in

the electricity sector. The dynamics in the renewable heating and cooling market sector may be

underestimated due to the more limited data available for this sector. Finally, the specific accounting rules

in the RED concerning renewables consumed in transport remain difficult to replicate. Despite these

challenges, the estimation of RES share proxies yields plausible results in most cases and should be further

improved, especially as more timely information and data that are relevant for the estimations become

available.

Gross avoided greenhouse gas emissions due to avoided fossil fuel use

Chapter 0 estimates the gross effects of renewable energy consumption on GHG emissions based on

primary data available from Eurostat for primary energy consumption in 2018. The term ‘gross avoided

GHG emissions’ illustrates the theoretical character of the GHG effects estimated in this way, as these

contributions do not necessarily represent ‘net GHG savings per se’ or are not based on life-cycle

assessment or full carbon accounting (

5

). Considering life-cycle emissions could lead to substantially

different results. It is important to note that, because the base year of this analysis is 2005, the

development of renewable energy from only that point in time is considered. Section 0 illustrates the

avoided fossil fuel use at the Member State level. The relative effects are shown with respect to gross

inland fossil fuel use per country (see Figure 20). Section 0 also estimates the effects on energy

consumption. A detailed description of the methodology applied for approximating these effects was

provided in a previous EEA report (EEA 2015).

Gross effect of renewable energy on air pollutant emissions

(

4

) The approximated GHG emissions, energy consumption and RES proxy data were sent for consultation to the

European Environment Information and Observation Network (Eionet) of environmental bodies and institutions

active in the EEA member countries. These proxies were finalised in October 2019, after the Eionet consultation.

(

5

) In the absence of specific information on current bioenergy systems, CO

2

emissions from the combustion of

biomass (in solid, liquid and gaseous forms) were not included in national GHG emission totals in this report, and

a zero emission factor had to be applied to all energy uses of biomass. This should not be interpreted, however,

as an endorsement of default biomass sustainability or carbon neutrality. It should be noted that, according to

the United Nations Framework Convention on Climate Change (UNFCCC) reporting guidelines, these emissions

have to be reported separately in GHG inventories as a memorandum item (mainly to avoid double counting of

emissions from a reporting perspective), with the assumption being that unsustainable biomass production

would show as a loss of biomass stock in the land use, land use change and forestry (LULUCF) sector and not in

the energy sector.

Eionet Report - ETC/CME 2019/8 10

Chapter 3 also estimates the gross effect of renewable energy consumption on air pollutant emissions.

Based on the gross final energy consumption of renewable energy technologies (RETs), the attributes of

individual RETs, the primary energy use per unit of electricity or heat, the implied emission factors

calculated with GAINS data, an estimate is made of the gross effect of renewable energy on air pollutant

emissions for the EU-28 and per Member State (ETC/CME 2019a; ETC/CME 2019b).

Renewable energy investments

To date, a central, publicly available source of information on global RES technology investments is missing.

The comprehensive information used in this assessment is sourced from the Global trends in renewable

energy investment annual report (Frankfurt School-UNEP 2019). The period covered is 2005-2018 and the

focus is on new renewable energy investments per region. While analysing investments, the report

includes projects on renewable power and fuels — wind, solar, biomass and waste, biofuels, geothermal

and marine projects, and small hydro-electric dams of less than 50 MW. It does not cover larger hydro-

electric dams of more than 50 MW. Investment figures were originally supplied in nominal billions of US

dollars. Full comparability across regions and time remains limited, as nominal values include inflation (

6

).

For the purpose of this report, figures in US dollars have been converted to euros using the Eurostat data

set on exchange rates (Eurostat 2019b).

Renewable energy employment

The renewable energy sector requires specific skills and value chains, which lead to the creation of new

jobs. Job numbers can be estimated using various methods with different levels of detail. As data

availability varies across regions and data differ as regards quality and methods, a consistent time series

is not yet available. For these reasons, only a snapshot of the recent past (2017), by available region and

technology, can be shown. Direct and indirect jobs related to renewable energy per region for 2017 are

presented below and stem from the International Renewable Energy Agency (IRENA 2019b).

Newly introduced Eurostat codes and descriptions

In January 2019, Eurostat introduced a novel methodology for the energy balances, mostly to harmonise

codes and labels with international statistics. Eurostat therefore established new specific indicators and

used those in the calculations: Gross Inland Consumption (Europe 2020-2030); Primary Energy

Consumption (Europe 2020-2030); Final Energy Consumption (Europe 2020-2030) (

7

). These indicators

flank the new GIC, PEC, and FEC indicators that are “[…] calculated to ensure continuity and transition from

the old Eurostat energy balance into the new Eurostat energy balance”.

The “Europe 2020-2030” indicators have been used exclusively when referring to total amounts, to check

the trend towards the 2020 targets. The other indicators have been used when breaking down the analysis

for specific fuels, e.g. fossil fuels. This distinction was needed for both the lack of data for single fuels in

the “Europe 2020-2030” indicators, as well as a more scientifically correct analysis for the fossil fuels

themselves. The related tables and figures will state which indicator has been used.

On another note, the “Combustible fuels” label does not exist anymore as a single indicator – but it is,

instead, now possible to calculate the indicators for the desired fuels. The full list of fuels included in the

calculations is presented below:

(

6

) To adjust for inflation one would need to consider individual inflation rates — or deflators — for each of the

regions. As the regions are composed of heterogeneous countries, probably experiencing different levels of

inflation, it is not possible to make this conversion. This needs to be taken into account when interpreting the

data.

(

7

) For the exact definition, refer to the official documentation.

Eionet Report - ETC/CME 2019/8 11

C0110

Anthracite

O4300

Refinery feedstocks

C0121

Coking coal

O4610

Refinery gas

C0129

Other bituminous coal

O4620

Ethane

C0210

Sub-bituminous coal

O4630

Liquefied petroleum gases

C0220

Lignite

O4640

Naphtha

C0311

Coke oven coke

O4652XR5210B

Motor gasoline (excluding

biofuel portion)

C0320

Patent fuel

O4661XR5230B

Kerosene-type jet fuel

(excluding biofuel portion)

C0330

Brown coal briquettes

O4671XR5220B

Gas oil and diesel oil

(excluding biofuel portion)

C0340

Coal tar

O4680

Fuel oil

P1100

Peat

O4694

Petroleum coke

P1200

Peat products

O4695

Bitumen

G3000

Natural gas

W6100

Industrial waste (non-

renewable)

O4100_TOT

Crude oil

W6220

Non-renewable municipal

waste

O4200

Natural gas liquids

Table 1 - List of fuels included in the calculations for Eurostat indicators

Other observations

For offshore wind, 2005-2017 data are calculated based on capacities reported by EurObserv’ER, while

2018 data are calculated on capacities reported by WindEurope. The decision to go for these sources

instead of Eurostat SHARES values came from the incompleteness of the information in the latter source.

All of the production calculations are based on an assumption of 4 000 full load hours of operation. The

offshore wind production is then subtracted from the total wind production reported by Eurostat (Eurostat

2019d) and the result is attributed to onshore wind production. The total of onshore and offshore wind

power generation is equal to the total for wind power reported by Eurostat. Data for 2020 originate from

table 10 in each country’s NREAP, where there is separate reporting for onshore and offshore wind power.

In the context of renewable energy use in transport the terms ‘other biofuels’ and ‘all biofuels’ are

understood to also include biogas and other liquid biofuels used in transport. Similarly, in the context of

RES-E generation, the term ‘solid biomass’ is understood to also include renewable municipal waste.

The methods applied in this report to estimate the impact of the uptake of renewable energy on energy

consumption and GHG emissions cannot be used to assign these effects to particular drivers,

circumstances or policies, other than the increased consumption of renewable energy itself. These

methodologies provide valuable insights, but as the assumptions are static (i.e. the same set of

assumptions is applied to all years in the period), assumptions need to be re-adjusted at times to reflect

real-life conditions. A detailed description of the methods was given in a previous report (EEA 2015).

Eionet Report - ETC/CME 2019/8 12

2 Developments in renewable energy sources in Europe

Key messages

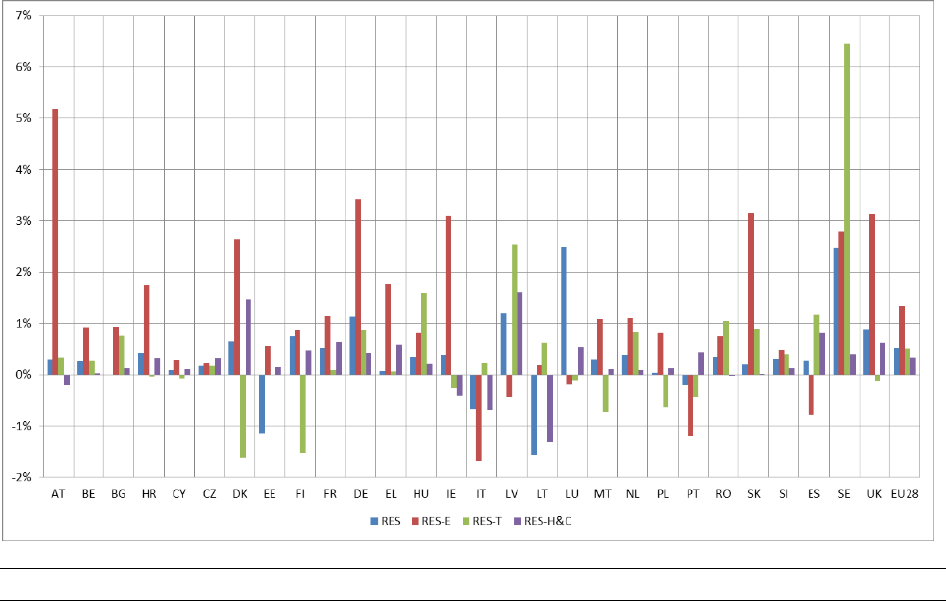

• The EU share of renewable energy in 2017 (17.5 %) was almost twice as high as in 2005 (9.1 %). However, it has

increased by only 0.5 percentage points since 2016.

• According to preliminary estimates calculated by the EEA, the EU’s RES share also continued to grow in 2018,

reaching an estimated 18.0 % share in gross final consumption (

8

).

• The EU RES share in both 2017 and 2018 exceeded the EU’s indicative trajectory under the RED (16.0 % in 2017

and 2018). However, reaching with certainty the mandatory 20 % EU RES share in energy consumption and the

10 % RES sub-target for transport by 2020 calls for continued efforts to deploy renewables and to address the

recent increases in energy consumption across some countries. Furthermore, ambitious national objectives and

the recalibration and adaptation of national RES support policies are indispensable in the short run, if we are to

meet the collective EU decarbonisation and energy targets for 2030 and in the longer term.

• On a per capita basis, the average RES-E capacity for the EU had more than doubled by 2017 (0.8 kWe per person)

compared with 2005. While differences between Member States remain large, in 23 EU countries installed RES-

E capacities per capita were larger than the world average (0.3 kWe per person) in 2017.

• Expressed per unit of gross domestic product (GDP) (

9

), the EU’s average RES-E capacity has developed in a similar

way since 2005, having more than doubled by 2017 (29 kWe per unit of GDP). Per unit of GDP, installed capacities

in 2017 were larger than the world average (24.6 kWe per unit of GDP) in 16 of the 28 EU Member States.

• Across the EU, in absolute terms, the largest market sector for renewable energy use remains heating and

cooling. Renewables made up close to one fifth of all final energy consumed for heating and cooling in the EU.

• Electricity is the second largest market sector for renewable energy use in the EU (RES-E share of 30.7 % in 2017

and 32.1 % in 2018 according to the early EEA estimates).

• Transport is the third and smallest market sector for renewables (7.6 % in 2017 and 8.1 %in 2018, according to

the early EEA estimates). Renewable energy use in transport (including only biofuels certified in accordance with

the existing sustainability criteria) varied significantly among Member States.

• Certain renewable energy technologies have already surpassed the levels of deployment expected for 2020 in

NREAPs, notably RES-H&C from solid biomass and RES-E from solar PV and biogas.

(

8

) The approximations are made using a harmonised method that can be applied to all Member States using

centrally available and harmonised data sets. It is not intended to be a tailor-made approach and the results

need to be considered with that in mind. Countries were invited to provide national data and estimates in the

context of an Eionet consultation in 2019. For details, see Annexes 3 and 4.

(

9

) GDP expressed in constant 2010 euro value (EUR

2010

), at purchasing power parity (PPP).

Eionet Report - ETC/CME 2019/8 13

2.1 Recent progress in deployment of renewable energy sources

2.1.1 Renewable energy shares at the EU level and in individual Member States

The RED (EU 2009) sets minimum indicative trajectories for each country, which end in the binding national

RES share targets for 2020. Progress towards these 2020 targets is assessed by comparing the most recent

developments with these interim trajectories. The indicative RED target for the EU is 13.8 % for the years

2015 and 2016 and 16 % for the years 2017 and 2018. Having achieved a RES share of 17.5 % in 2017 and

an estimated share of 18.0 % in 2018, the EU has surpassed the indicative target level set in the RED.

The RES share increased annually by 8 percentage points, on average, between 2005 and 2017, with the

pace of growth decreasing in 2016 and 2017 (to 2 and 3 percentage points, respectively). It is worth noting

that gross final energy consumption decreased between 2005 and 2017 by 0.5 percentage point, on

average, but it increased in 2015, 2016 and 2017, with respectively 2, 2 and 1 percentage points,

respectively. According to early EEA estimates, final energy consumption continued to increase by 0.1 %

in 2018 compared to 2017. As shown elsewhere, the slowdown in the annual increase in the RES share in

recent years was due to the increase in final energy consumption in recent years. If this latter trend is not

reversed, it could jeopardise the achievement of the 20 % renewable energy target at EU level for 2020

(EEA 2019). In addition, the current average pace of renewable energy deployment across Europe would

not enable the EU to achieve the new RES target, of 32 % by 2030. Meeting the more ambitious EU-level

RES (and climate mitigation) targets for 2030 and 2050 calls for steeper deployment rates of RES across all

sectors and especially in heating and cooling, and in transport (EEA 2019).

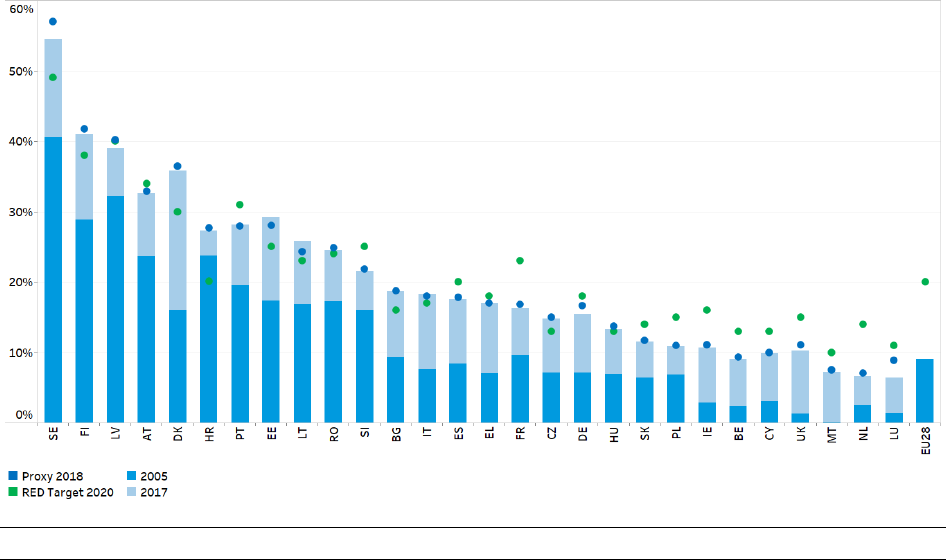

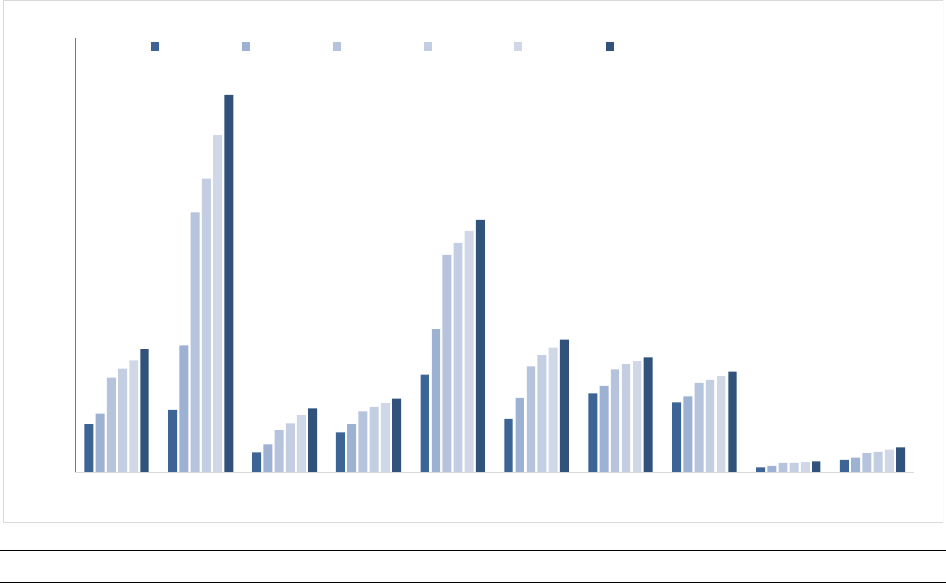

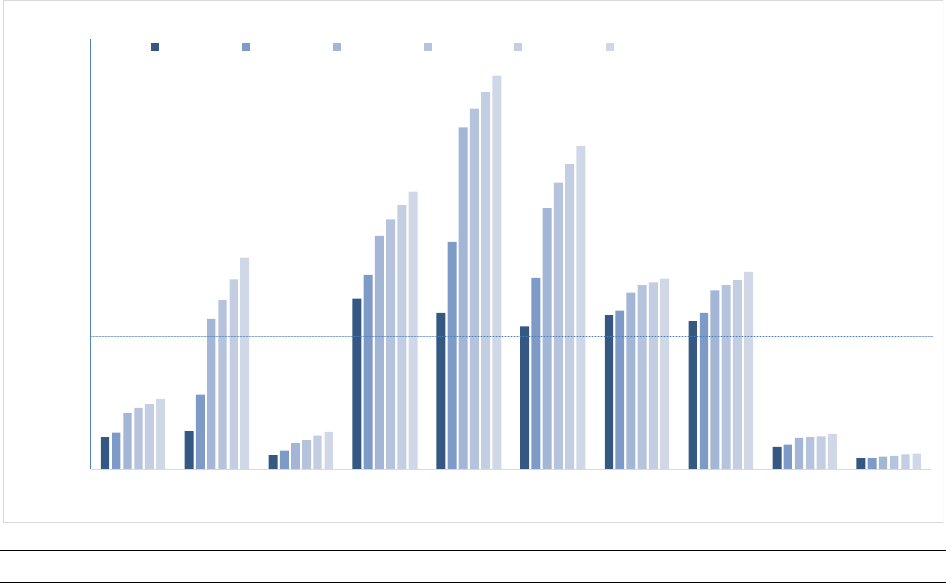

Figure 2 shows the actual RES shares in the EU Member States and for the EU for 2005 and 2017. The RES

shares vary widely among countries. In 2017, the highest shares of renewable energy were attained by

Sweden (54.5 %), followed by Finland (41.0 %) and Latvia (39.0 %). Luxembourg (6.4 %), the Netherlands

(6.6 %) and Malta (7.2 %) realised the lowest shares. Figure 2 also shows the RED target share for 2020.

This overall target was calculated for individual Member States to reflect their national circumstances, RES

potentials and starting points.

Eionet Report - ETC/CME 2019/8 14

Figure 2 Actual and approximated RES shares in the EU and its Member States

Notes: The dark blue bars show the RES shares in 2005. The tops of the light blue bars show the levels that the RES shares reached

in 2017

Sources: ETC/CME, (EEA 2018a); (Eurostat 2019d); RED (2009/28/EC).

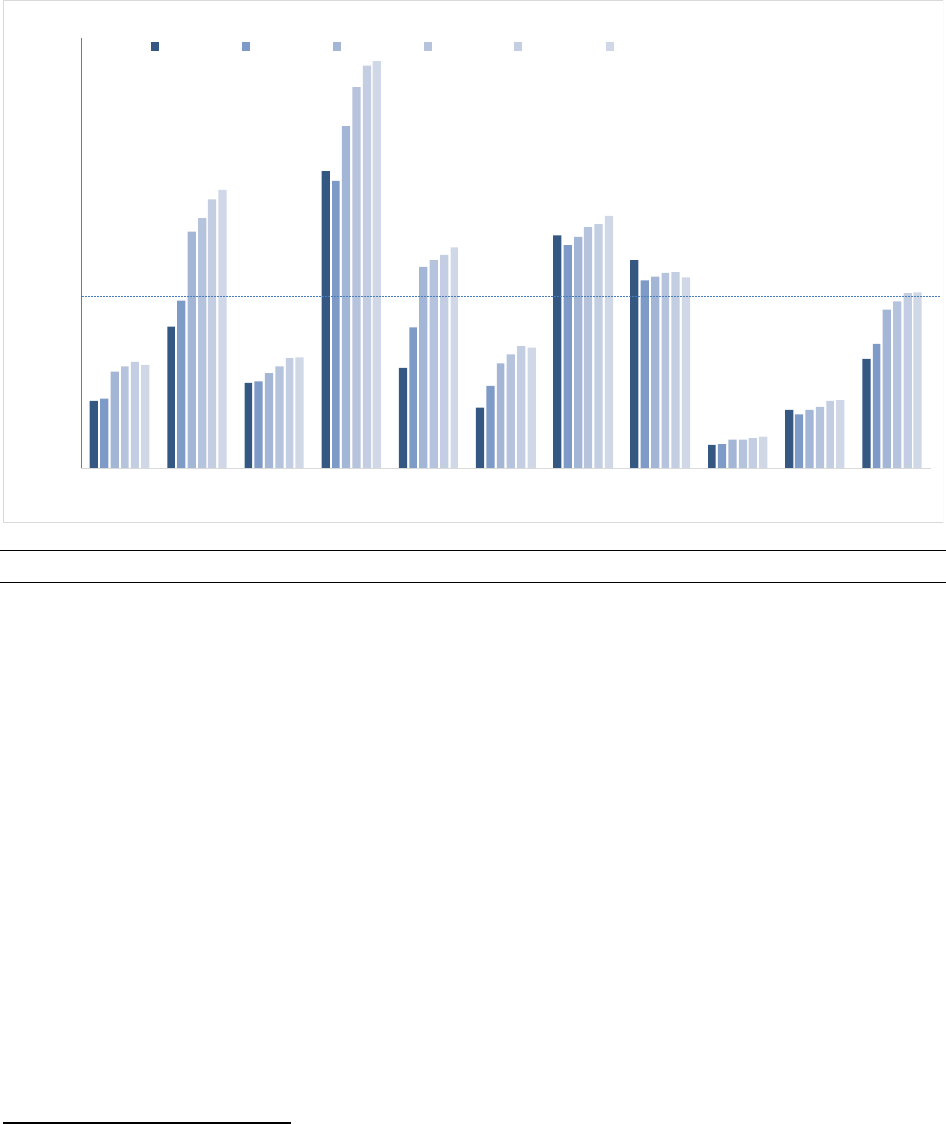

2.1.2 Renewable electricity capacities per capita and per unit of gross domestic product

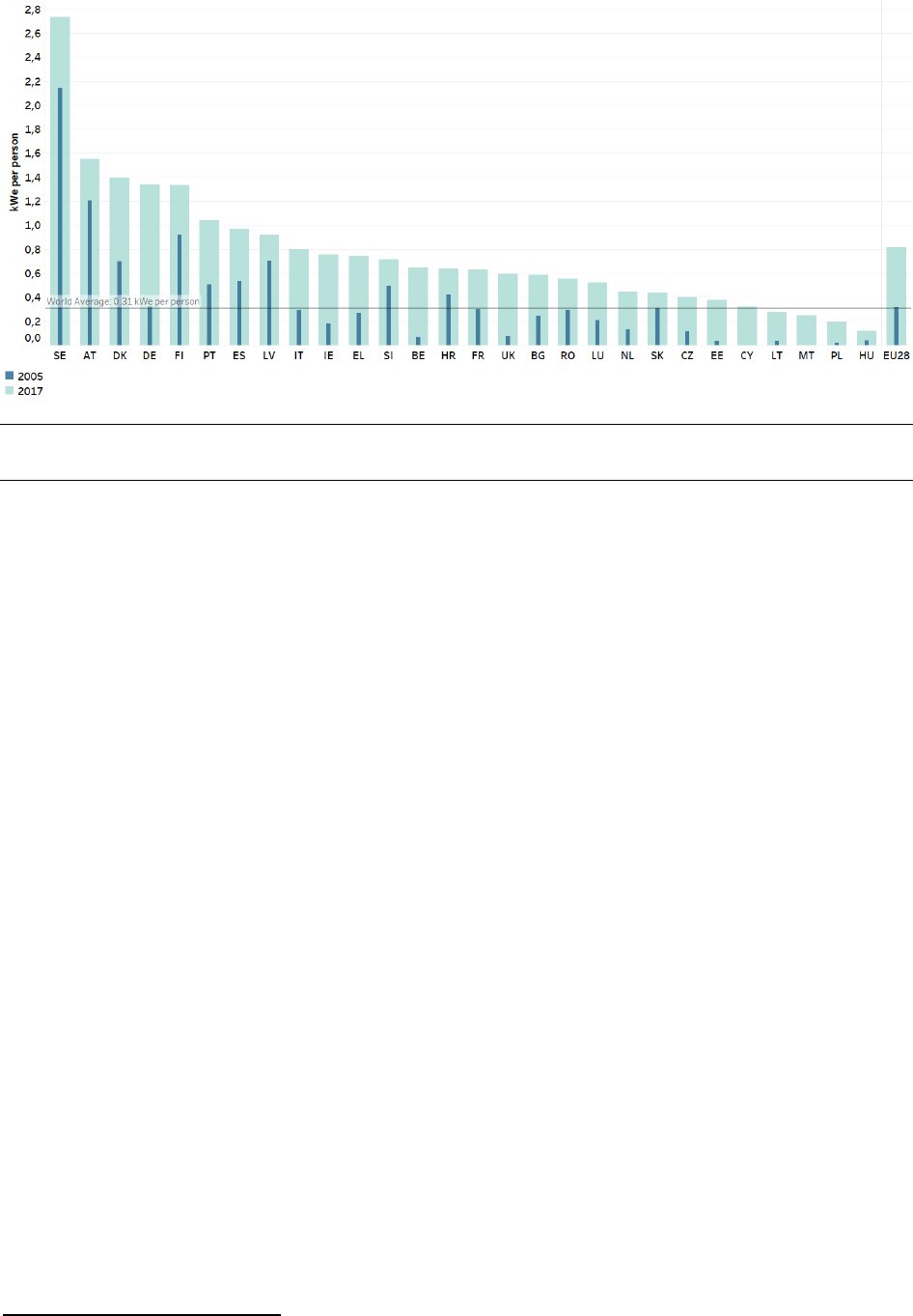

The average RES-E capacity per capita for the EU-28 had more than doubled by 2017, compared with 2005,

from around 0.3 kWe installed per person in 2005 to over 0.8 kWe installed per person in 2017. Sweden

had the largest installed capacity per person in 2017 of 2.7 kWe installed per person, followed at a distance

by Austria, Denmark, Germany and Portugal (1.3 to 1.6 kWe per person). However, since 2005, the largest

growth in RES-E capacity per capita has been observed in Malta, Cyprus, Estonia, Poland, Belgium, the

United Kingdom, Lithuania, Ireland, Germany, the Czech Republic and the Netherlands (all more than

300 % growth), followed by Hungary, Greece, Italy, Luxembourg, Bulgaria, France, Portugal and Denmark

(growth between 200 % and 300 %). The remaining countries (Romania, Spain, Croatia, Finland, Slovenia,

Slovakia, Latvia, Austria and Sweden) showed lower growth rates (< 200 %). The majority of EU Member

States (23) had installed capacities in 2017 that were greater than the world average (see Figure 3 and

Figure 32).

Eionet Report - ETC/CME 2019/8 15

Figure 3 RES-E capacities, excluding pumped storage, per capita in the EU and its Member States, 2005

and 2017

Sources: ETC/CME, (Eurostat 2019d), (Eurostat 2019c); (IRENA 2019a)

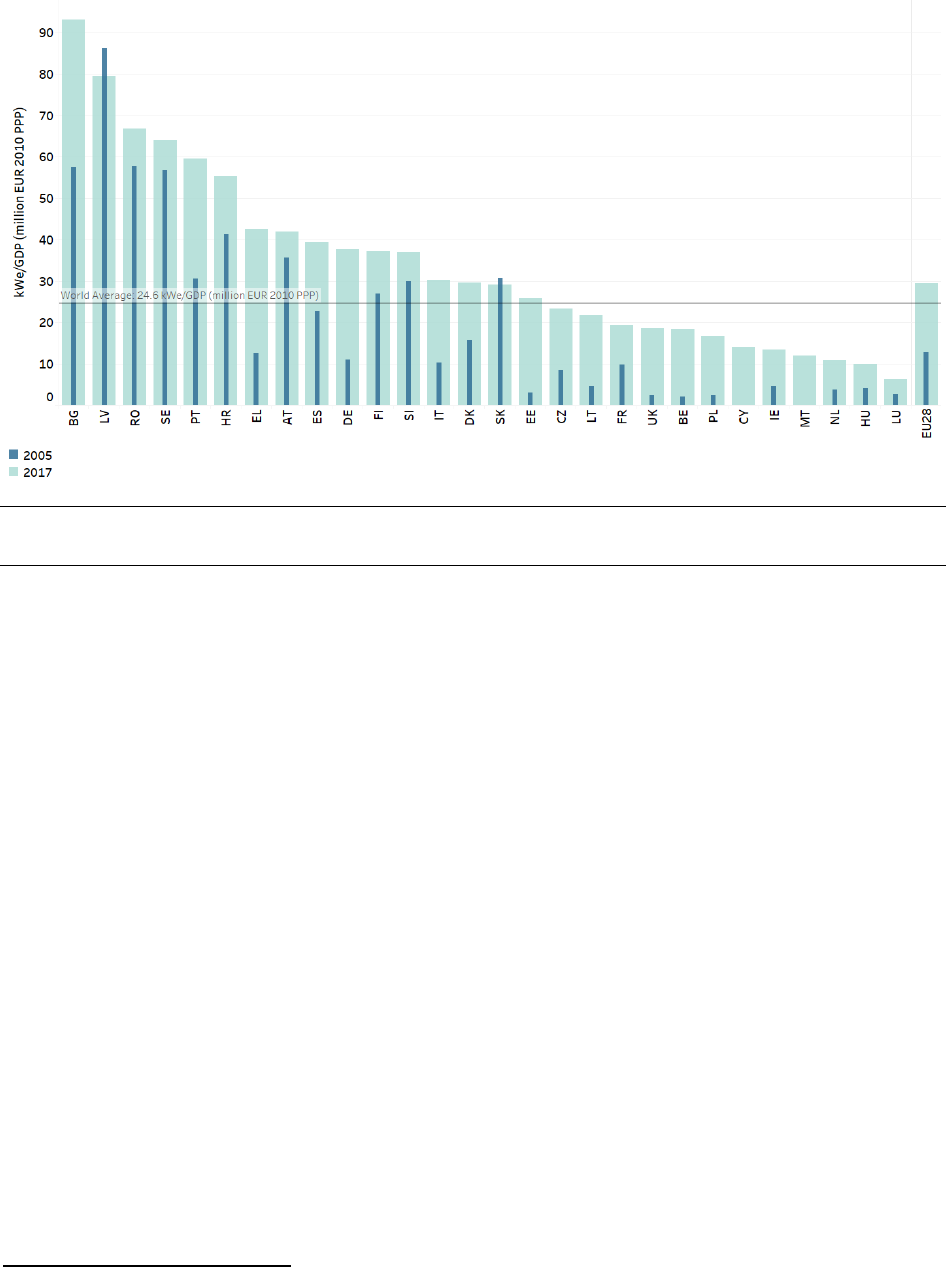

Similar to the average RES-E capacity per capita, the average RES-E capacity per unit of GDP for the EU-28

has more than doubled since 2005, reaching 29 kWe/GDP (

10

) in 2017. In 2017, Bulgaria, Latvia and

Romania had the largest installed capacities per unit GDP (65 kWe/million EUR

2010

(PPP) or more) followed

by Sweden, Portugal, Croatia, Greece and Austria (40 to 65 kWe/million EUR

2010

(PPP)). The largest growth

in RES-E capacity per GDP since 2005 can be observed in Malta, Cyprus, Belgium, Estonia, the United

Kingdom, Poland and Lithuania (all more than 450 % growth), followed by Germany, Greece, Ireland, the

Netherlands, Italy, Czech Republic, Hungary and Luxembourg (between 200 % and around 350 % growth).

The remaining countries (France, Portugal, Denmark, Spain, Bulgaria, Finland, Croatia, Slovenia, Austria,

Romania, Sweden, Slovakia and Latvia) showed lower growth rates (< 200 %) per unit of GDP. Per unit of

GDP, installed capacities in 2017 were larger than the world average (24.6 kWe per unit GDP) in 16 of the

28 EU Member States (see Figure 33).

(

10

) GDP expressed in constant 2010 euro value (EUR

2010

) at PPP.

Eionet Report - ETC/CME 2019/8 16

Figure 4 RES-E capacities, excluding pumped storage, per GDP in the EU and its Member States, 2005

and 2017

Sources: ETC/CME; (Eurostat 2019d); (IRENA 2019a);(Eurostat 2019b).

2.2 Contributions of renewable energy sources by energy market sector and technology

In 2010, Member States submitted NREAPs in which they outlined their expected national paths to meet

their binding 2020 RES targets and included separate trajectories for RES-E, RES-H&C and renewable

energy consumption in the transport sector (RES-T). The expected paths in the NREAPs are, overall, more

ambitious than the indicative RED trajectories. This section shows the progress achieved by RES within the

three energy market sectors and compares it with the expected (NREAP) development in these market

sectors.

The expected (NREAP) trajectories of individual technologies enable progress to be monitored, but they

become increasingly outdated as conditions and policies change (

11

). In fact, because of steep learning

curves, the rapid development and consequent cost reductions achieved by some renewable energy

technologies have already led to higher shares of these technologies than were anticipated to have been

reached by 2020 in the NREAPs.

At EU level, in absolute terms RES-H&C remains the dominant RES market sector (see Section 2.2.3),

followed by RES-E (see Section 2.2.2) and RES-T (see Section 2.2.4).

2.2.1 Contribution of renewable energy sources to various energy market sectors in Member States

At the country level, the significance of each energy market sector, and the role renewable energy plays

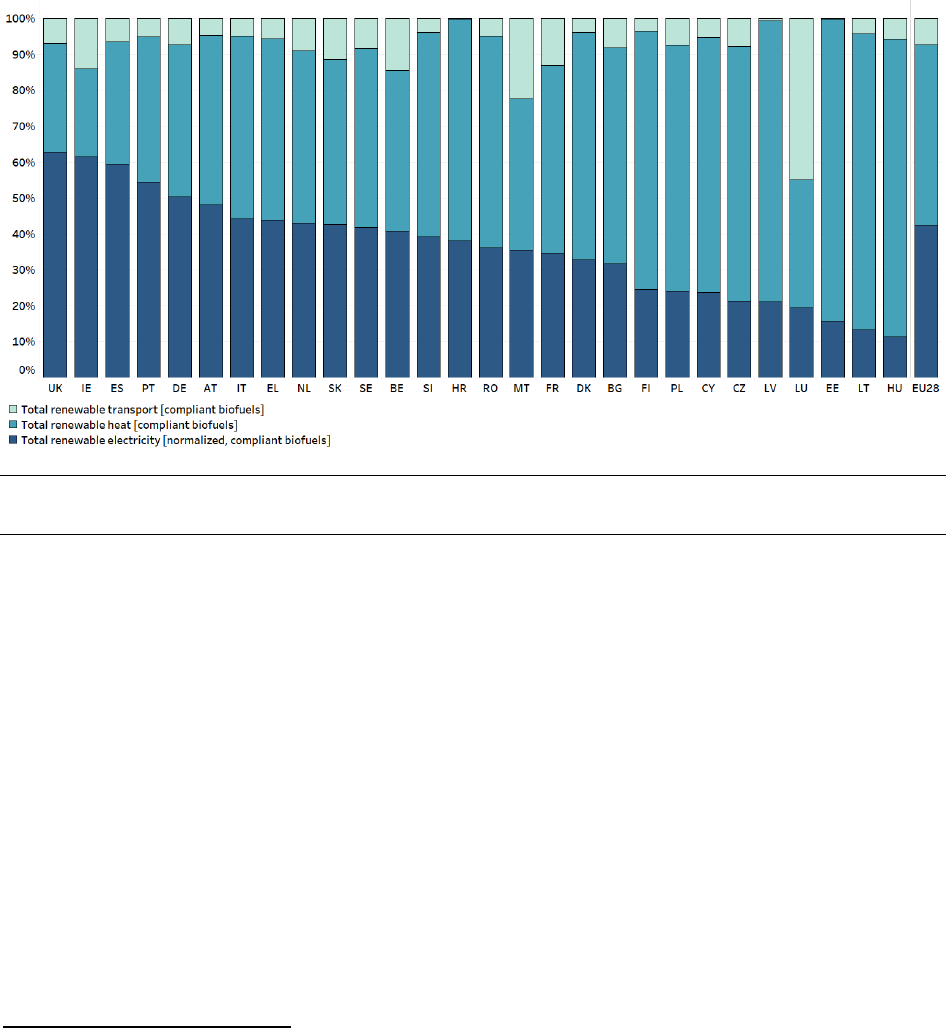

therein, differs considerably. Figure 5 Shares in 2017 RES consumption of renewable electricity, renewable

heating and cooling, and biofuels in transport illustrates these differences by showing the split of gross

final renewable energy consumption by market sector in each country. In 2017:

(

11

) Some countries have updated their NREAPs since 2010. The most recent versions were used for this report.

Austria, Bulgaria, Czech Republic, Denmark, Estonia, Ireland, Poland, Spain and Sweden updated their overall

RES shares, or their RES shares per technology, for one or several years, as additional information to the

Commission's questions or in a resubmission of their NREAP. The latest version of Malta’s NREAP is from 2017

and this version was used for this report.

Eionet Report - ETC/CME 2019/8 17

• Renewable heating and cooling represented more than half of all gross final consumption of

renewables in 16 Member States (Bulgaria, Croatia, Cyprus, Czech Republic, Denmark, Estonia,

Finland, France, Greece, Hungary, Italy, Latvia, Lithuania, Poland, Romania and Slovenia).

• Renewable electricity represented over half of all RES consumption in only five countries (in

descending order: the United Kingdom, Ireland, Spain, Portugal and Germany).

• The contribution of renewable transport fuels (certified biofuels) was on average 7.3 %, but varied

significantly among Member States from a maximum of 45 % of all RES consumption (Luxembourg) to

less than 1 % (Croatia, Estonia and Latvia).

Figure 5 Shares in 2017 RES consumption of renewable electricity, renewable heating and cooling, and

biofuels in transport

Notes: This figure shows how actual final renewable energy consumption in 2017 is distributed over RES-E, RES-H&C and biofuels

in transport. Wind power and hydropower are normalised (

12

). The consumption of RES accounts for only biofuels complying with

the RED sustainability criteria.

Source: Compiled from data in (Eurostat 2019d).

The variations observed across countries in the relative importance of each market sector are due to

specific national circumstances, including different starting points in terms of the deployment of RES,

different availability of low-cost renewables, country-specific demand for heating in the residential sector

and different policies to stimulate the deployment of renewable energy.

2.2.2 Renewable electricity

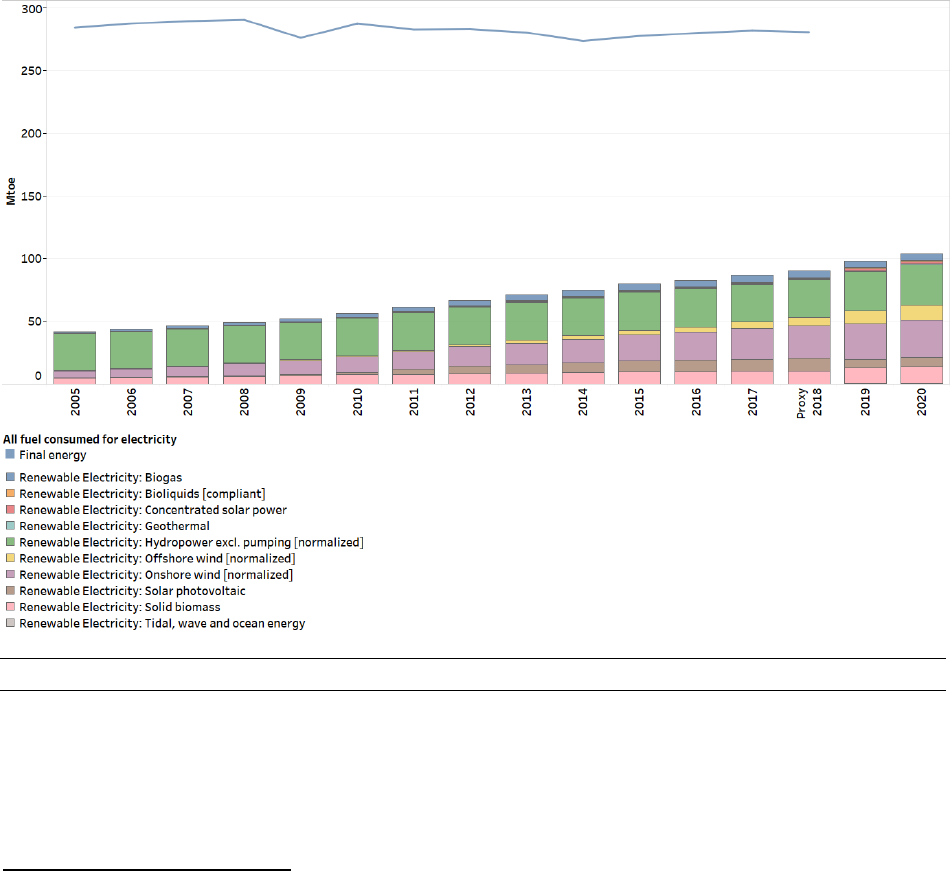

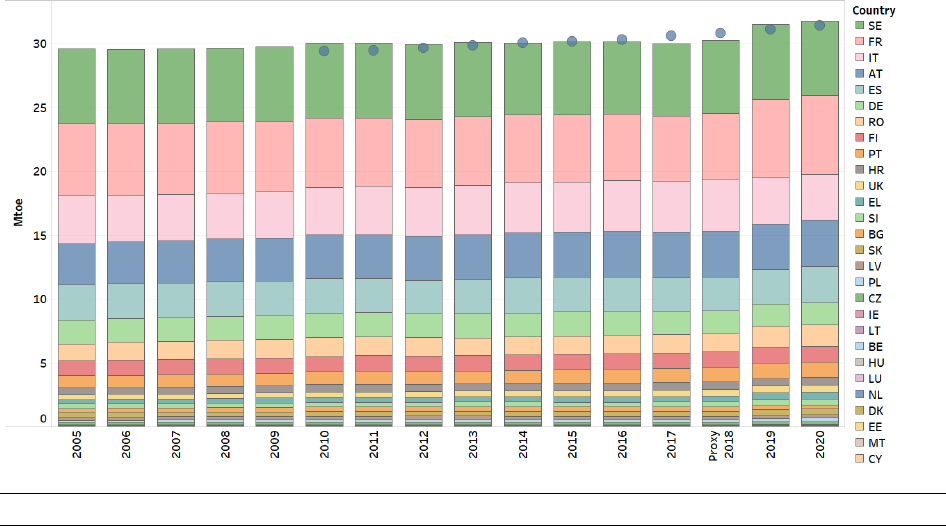

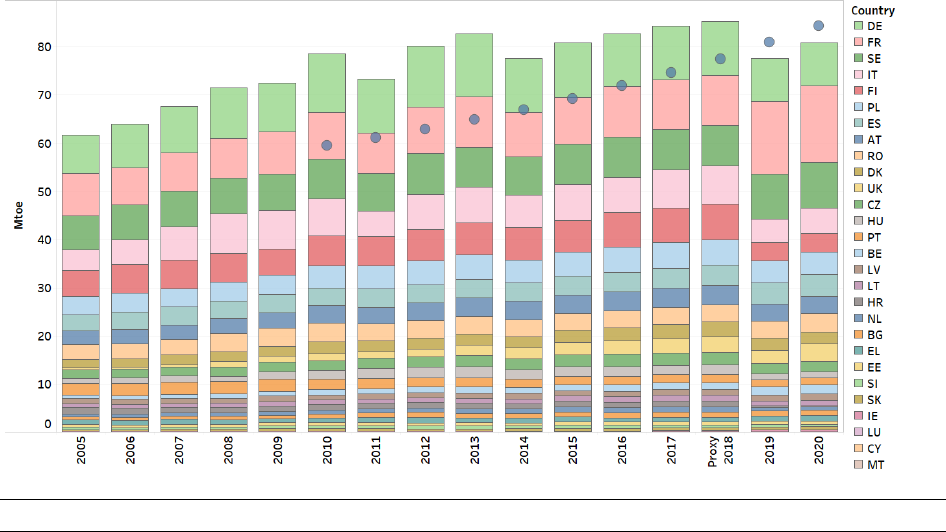

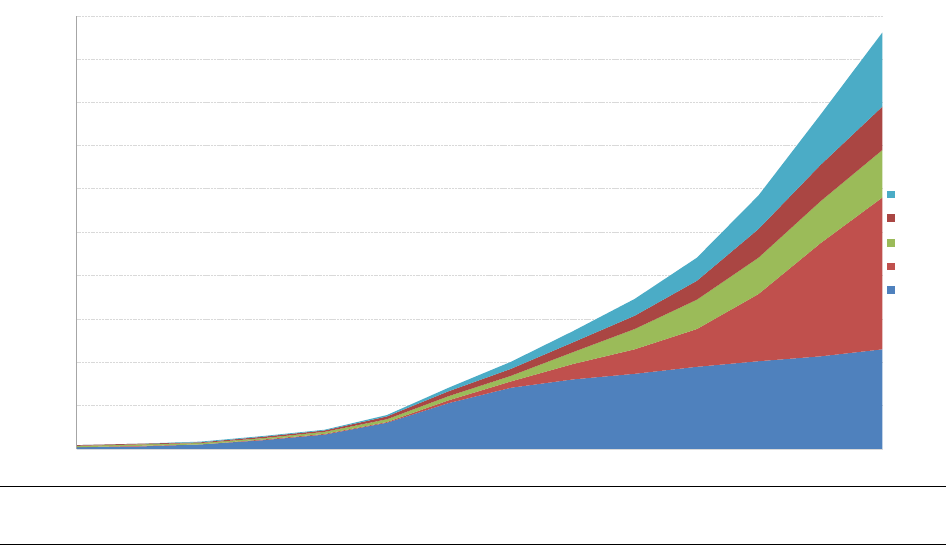

In 2017, the EU-wide share of RES-E amounted to 30.7 % — more than twice the level in 2005. Figure 6

RES-E in the EU and Table 2 RES-E in the EU, by RES technology show the consumption of RES-E up to 2017,

approximated estimates for 2018 and the expected NREAP developments by 2020.

• The gross final energy consumption of RES-E continued to increase, reaching 86.7 Mtoe in 2017.

(

12

) Under the accounting rules in the RED, electricity generated by hydro- and wind power needs to be normalised

to take into account annual climatic variations (hydro for 15 years and wind for 5 years).

Eionet Report - ETC/CME 2019/8 18

• In 2017, the largest contributions came from hydropower and wind power (35 % and 34 % of all

RES-E, respectively) (

13

), solid biomass (12 % of all RES-E) and solar PV systems (11 % of all RES-E).

All the other technologies made smaller contributions, ranging from 0.1 % (tidal, wave and ocean

energy) to 6 % (biogas).

• Over the period 2005-2017, the RES-E consumption increased by 9 percentage points per year, on

average. To achieve the expectations for 2020 in the NREAPs, an increase by 7 percentage points

per year, on average, will be required over the period 2017-2020. For 2005-2017, the increase was

the highest for solar PV systems, offshore wind, biogas and onshore wind with respectively 637,

158, 33 and 28 percentage points increase per year, on average. For the same period, hydropower

had the lowest increase with 0 percentage points per year, on average.

According to EEA early estimates, RES-E generation increased in 2018 to 90.5 Mtoe, while total electricity

generation from all sources increased to 280.7 Mtoe, resulting in a RES-E share of 32.1 %. Most of the

increase in RES-E generation in 2017 was due to the greater contribution of wind energy (+3.1 Mtoe) and

solar energy (+0.7 Mtoe). In 2017, electricity consumption in Europe increased for the third consecutive

year following the decrease in 2014.

Figure 6 RES-E in the EU

Notes: This figure shows the actual final RES-E consumption for 2005-2017, approximated estimates for 2018 and the expected

realisations in the energy efficiency scenario of the NREAPs for 2019-2020. Wind power and hydropower are normalised. The

consumption of RES accounts for only biofuels complying with the RED sustainability criteria.

Sources: ETC/CME; Eurostat, (Eurostat 2019d); NREAP reports.

(

13

) The SHARES tool contains only total offshore and onshore wind energy production. In this report, it is assumed

that offshore wind turbines realise 4 000 full load hours per year. Accordingly, onshore and offshore wind

reached each a share of 28 % and 6 % of all RES-E, respectively.

Eionet Report - ETC/CME 2019/8 19

Notes: This table shows the actual final renewable energy consumption for 2005, 2016 and 2017, approximated estimates for

2018 and the expected realisations in the energy efficiency scenario of the NREAPs for 2020. Also shown are the average

percentage point increase per year for the period 2005-2017, the percentage point increase from 2016 to 2017 and the average

percentage point increase per year required to reach the expected realisations in the NREAPs for 2020. Wind power and

hydropower are normalised.

(a) Renewable municipal waste has been included in solid biomass.

(b) The series includes all biofuels and bioliquids consumed for electricity purposes, including uncertified ones after

2011.

Sources: ETC/CME; (Eurostat 2019d); NREAP reports.

Final energy (ktoe)

Percentage increase per year

Technology

2005

2016

2017

Proxy

2018

NREAP

2020

2005 -

2017

2016 -

2017

2017 -

2020

Hydropower excl.

pumping (normalised)

29 587

30 176

30 002

30 248

31 786

0 %

-1 %

2 %

Onshore wind

(normalised)

5 667

22 483

24 374

26 017

30 303

28 %

8 %

8 %

Solid biomass (

a

)

4 473

9 713

10 041

10 211

13 460

10 %

3 %

11 %

Solar PV systems

126

9 101

9 760

10 469

7 062

637 %

7 %

-9 %

Biogas

1 105

5 443

5 515

5 599

5 493

33 %

1 %

0 %

Offshore wind

(normalised)

273

4 267

5 441

6 362

11 740

158 %

28 %

39 %

Geothermal energy

464

584

583

586

943

2 %

0 %

21 %

Concentrated solar

power

0

480

506

530

1 633

n.a.

5 %

74 %

Bioliquids (certified)

0

440

415

415

1 096

n.a.

-6 %

55 %

Tidal, wave and ocean

energy

41

43

45

48

559

1 %

5 %

381 %

Total RES-E (normalised,

certified biofuels)

42 007

82 730

86 682

90 483

104 075

9 %

5 %

7 %

Total RES-E (normalised,

including all biofuels) (

b

)

42 159

82 745

86 696

90 498

104 075

9 %

5 %

7 %

Table 2 RES-E in the EU, by RES technology

Eionet Report - ETC/CME 2019/8 20

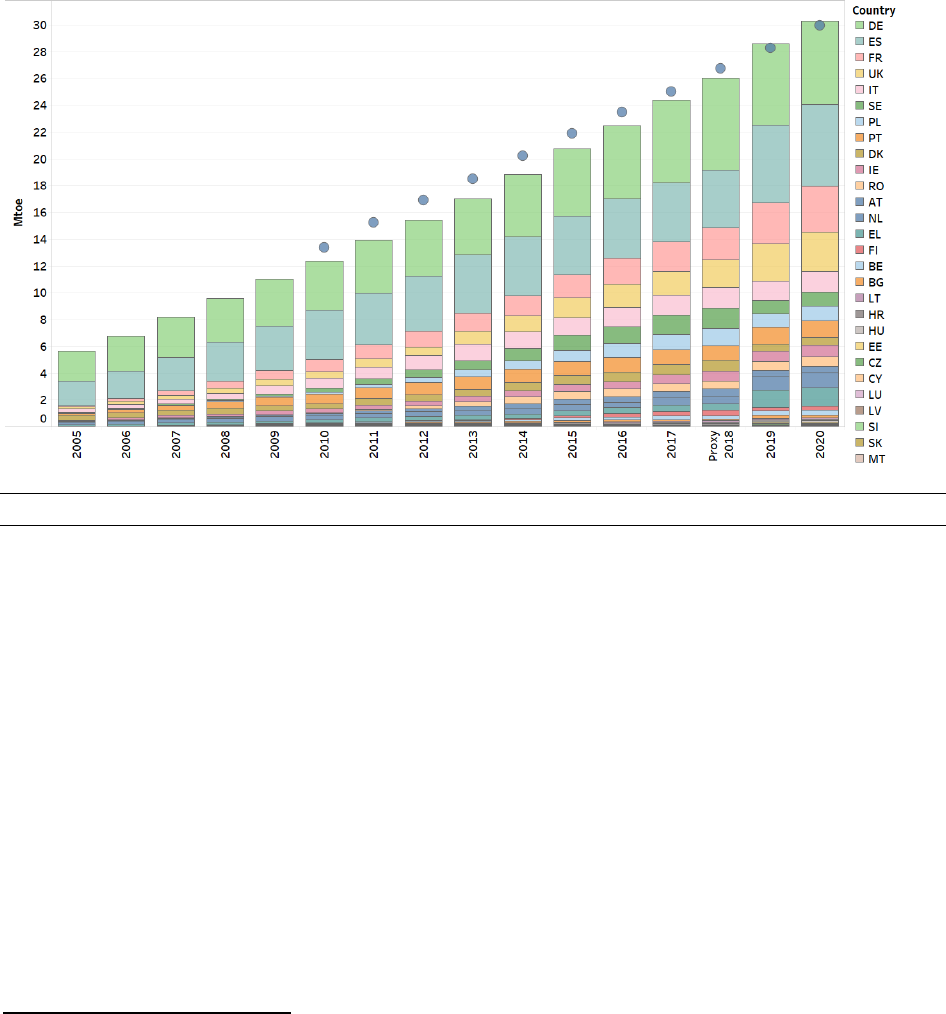

Hydropower

Rainfall patterns determine annual changes in hydroelectricity production. That is why normalised

production data are taken into account. The normalised (

12

) production of renewable hydroelectric power

remained quite stable over the period 2005-2017, but in 2017, the normalised production of

hydroelectricity has decreased slightly, from 30.2 Mtoe in 2016 to 30.0 Mtoe as illustrated in Figure 7.

According to the NREAPs, limited growth, from 30.0 to 31.8 Mtoe, is expected for the period 2017-2020.

In 2017, the five countries with the most hydropower (Sweden, France, Italy, Austria and Spain) had a

share of 70 % of all hydropower generation in the EU. In 2018, the normalised production of

hydroelectricity is likely to increase in absolute value (from 30.0 Mtoe in 2017 to 30.2 Mtoe in 2018), but

decreasing its share (from 35 % in 2017 to 33 % in 2018).

Hydropower is a flexible, mature technology for power generation, and hydropower reservoirs (dams) can

provide energy storage. Investments in large-scale hydropower (> 10 MW) were mainly made before 2000.

Most of the best sites have already been developed (amounting to about half of the technically feasible

potential; Pedraza, 2014), which is why hydropower capacities evolve only a little across Europe. In 2018,

the largest capacities (including pumped storage) have been added in Austria, Iceland and Italy

(respectively 385, 100 and 88 MW). Much larger capacities were added outside the European Union, in

Turkey and Norway (respectively 1 085 and 419 MW) (International Hydropower Association 2019).

For large-scale hydropower (> 10 MW), the difference between expected and planned electricity

generation is relatively small compared to other RES-E technologies. Based on modelling results with

Green-X (

14

), at EU level, a relatively low underachievement, of ca. 5 % compared to the NREAP trajectory

for this technology, is expected for 2018. For 2020, it is expected that the situation remains rather the

same, with large-scale hydropower ending up below the target, with a relatively small deviation of 6.7 %.

For small scale hydropower a slight overachievement by 2018 (of 2.3 % to 3.4 %) and a slight

underachievement till low overachievement (-0.4 % to 1.3 %) by 2020 is expected (Ecofys 2019).

Hydropower projects may negatively impact the habitats where they are installed and its operation cause

mortality of several flying species (namely birds, bats, butterflies). In order to minimise such impacts, the

European Commission published guidance for use by competent authorities, developers and consultants

‘The requirements for hydropower in relation to EU Nature legislation’ (EC 2018).

(

14

) The Green-X model allows the investigation of the future deployment of RES as well as the accompanying costs

and benefits. Results are calculated at both country- and technology-level on a yearly basis. Two scenarios were

modelled: Current Policy Initiatives (CPI) and Current and Planned Policies Initiatives (CPI + PPI) (Ecofys 2019).

Eionet Report - ETC/CME 2019/8 21

Figure 7 RES-E in EU hydropower excluding pumping (normalised)

Notes: This figure shows the actual final RES-E consumption for 2005-2017, approximated estimates for 2018 and the expected

realisations in the energy efficiency scenario of the NREAPs for 2019-2020.

Sources: ETC/CME; (Eurostat 2019d); NREAP reports.

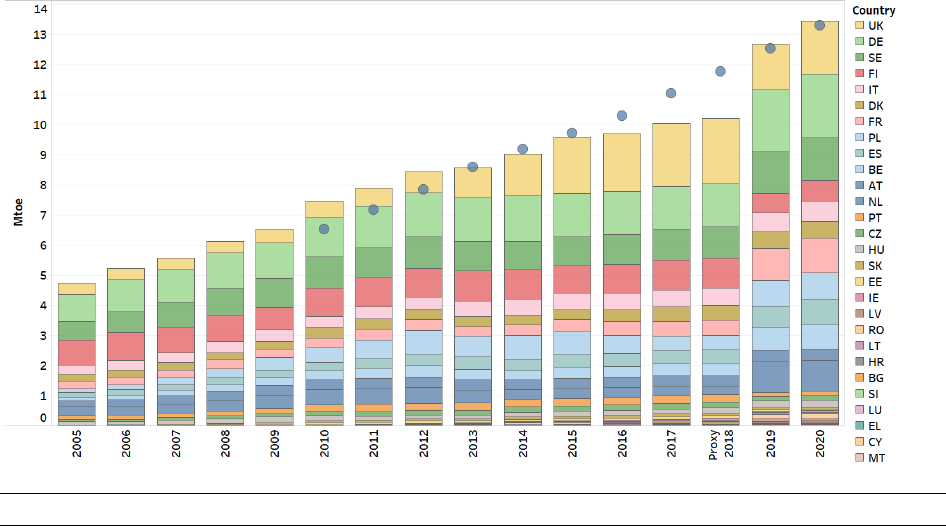

Onshore wind

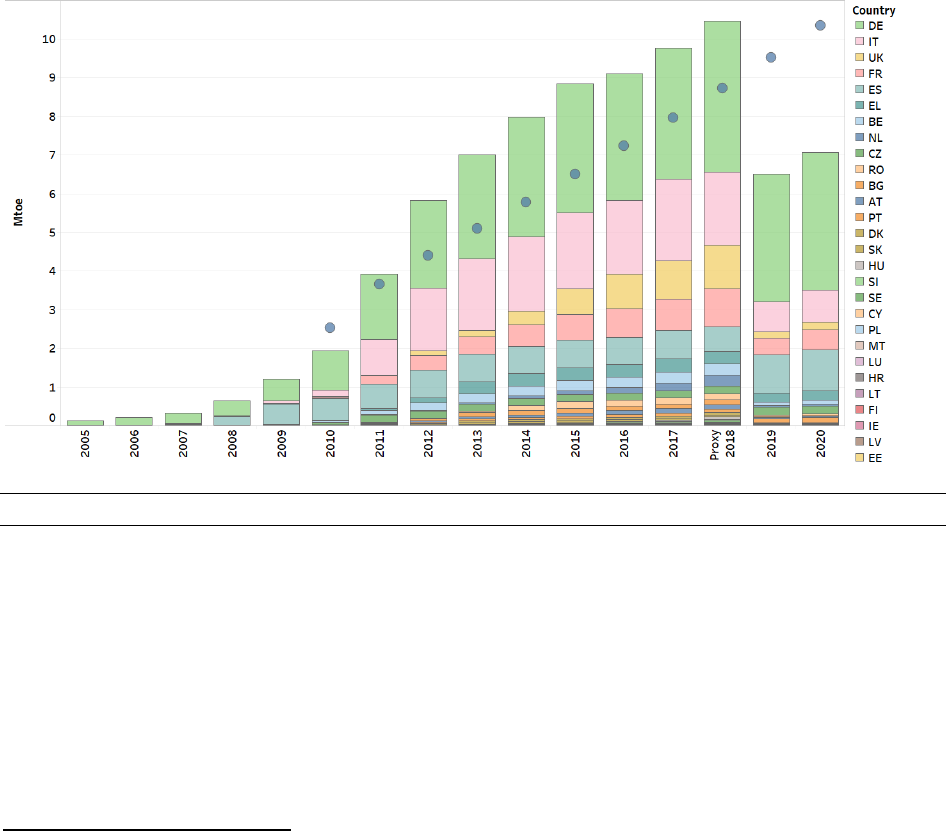

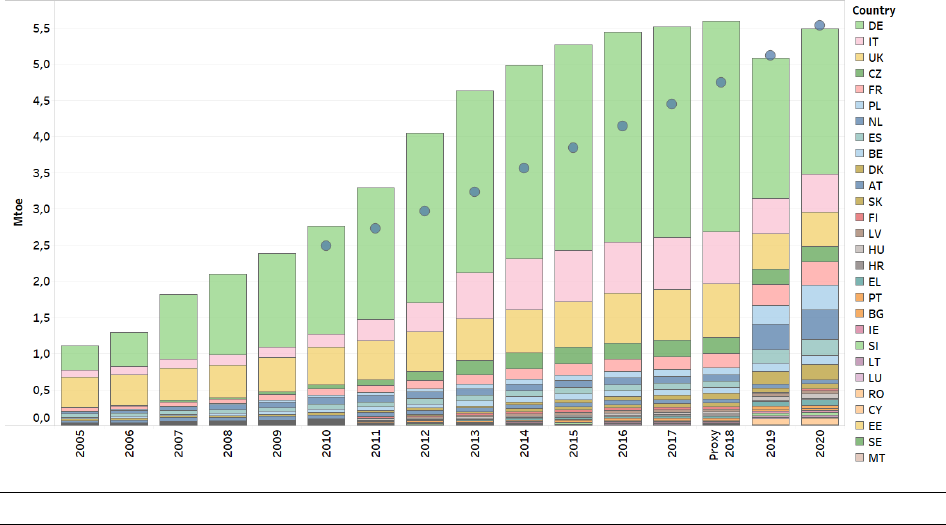

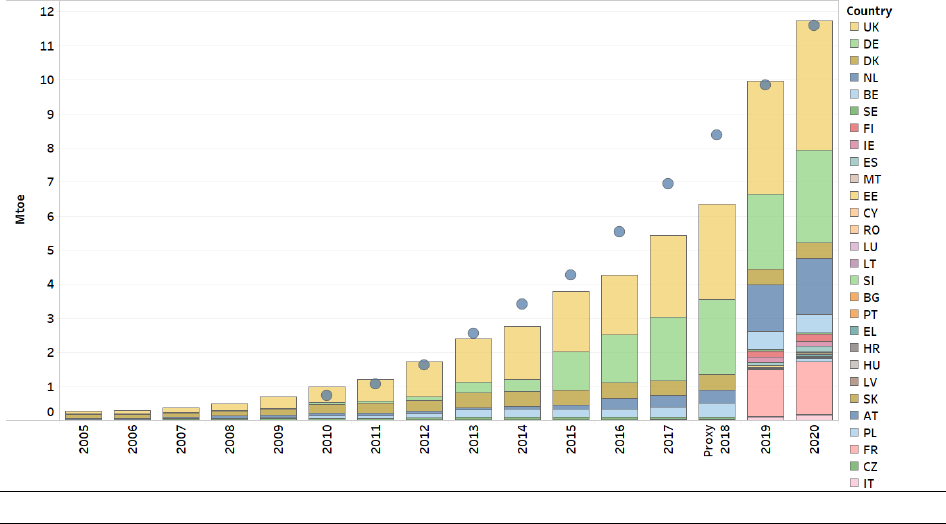

Onshore wind power generation increased from 5.7 Mtoe in 2005 to 24.4 Mtoe in 2017. The largest

increases came from Germany (6.2 Mtoe in 2017) and Spain (4.4 Mtoe in 2017).

In 2018, the normalised

(12)

onshore wind production of electricity is estimated to reach 26.0 Mtoe (Figure

8Figure 8 RES-E in the EU: onshore wind (normalised)).

Onshore wind is a rather mature and lower cost RES technology ((IRENA 2016); (Roland Berger 2016)). The

NREAPs indicate that onshore wind could increase to 30.3 Mtoe in 2020. Over the period 2005-2017

onshore wind increased by 28 percentage points per year, on average. Although an increase of

8 percentage points per year, on average, in the period up to 2020 would be sufficient to meet

expectations in the NREAPs, in reality wind power could continue to grow more rapidly until 2020, given

the cost reductions that have taken place over the past 10 years.

In 2018, the greatest annual increase in normalised onshore wind production at the Member State level

was recorded in Germany, followed by the United Kingdom and France. Germany was again the largest

installer, with 2.4 GW additional onshore capacity (not including 0.25 GW decommissioned) but this was

less than half of the 5.3 GW it installed in 2017. The main reasons for this slowdown in deployment were

the lengthy permitting procedures due, i.a., to objections resulting in legal proceedings and the fact that

a large proportion of the tender volumes has been won by ‘citizen’s projects’ that benefit from longer lead

times. France had its second best year, with 1.5 MW net installed in 2018. With its draft of a multi-year

energy programme (PPE) published at the start of 2019, France lays the foundation for investments in the

next decade (EurObserv’ER 2019; Wind Europe 2019).

Further developments on the wind energy market in general include concentration of manufacturers by

mergers and acquisitions and a thorough digitalisation of data transferring, sharing and processing to a

virtual world. According to EurObserv’ER, the general slowdown in installation rates reveals a need for

Power Purchase Agreements (PPAs), to enable wind producers to get involved in private sales contracts

directly. To follow on this aspect, the European Commission has asked Member States to set up a

regulatory framework that could promote PPAs in their forthcoming national action plans (EurObserv’ER

2019c). In 2018, 0.4 GW of wind power were decommissioned which is a decrease compared to 2017

(0.6 GW). A part of the decommissioned turbines were repowered and together with a part of

decommissioned capacity in 2017 it resulted in a total of 0.5 GW repowered capacity (Wind Europe 2019).

Eionet Report - ETC/CME 2019/8 22

Compared to the NREAP trajectory at EU level, for wind onshore a small gap in the range of 0.3 % to 5.0 %

is expected by 2018 and a similar situation by 2020 when the gap may increase to about 6.3% (Ecofys

2019).

In a number of countries, planned policy initiatives and optimistic framework conditions positively

influence progress in achievement of the sectoral trajectory. However, several other Member States are

expected to fail in achieving their trajectory but to a less significant extent and improvements related to

support as well as to market integration are required (Ecofys 2019).

To overcome the barrier of siting wind projects in such a way that they are compatible with protecting

biodiversity and Europe’s natural heritage, the European Commission developed the guidance ‘Wind

energy developments and Natura 2000’ (EC 2011))(EC 2001). It includes guidelines on how best to ensure

that wind energy developments are compatible with the provisions of the Habitats and the Birds Directives

(EC 2014).

Figure 8 RES-E in the EU: onshore wind (normalised)

Notes: This figure shows the actual final RES-E consumption for 2005-2017, approximated estimates for 2018 and the expected

realisations in the energy efficiency scenario of the NREAPs for 2019-2020.

Sources: ETC/CME; (Eurostat 2019d); NREAP reports.

Solid biomass

Electricity generation from solid biomass grew from 4.5 Mtoe in 2005 to 10.0 Mtoe in 2017, driven by,

inter alia, the expansion in biomass cogeneration and the conversion of coal-fired power plants to biomass

installations (

15

). The increase per year for the period 2005-2017 was by 10 percentage points per year, on

average (Figure 9). Since 2015, the United Kingdom has surpassed Germany in total electricity generated

from solid biomass. In 2017, it accounted for 21 % of total electricity generated from solid biomass and